Welcome to Fintech Brainfood, the weekly deep dive into Fintech news, events, and analysis. You can subscribe by hitting the button below, and you can get in touch by hitting reply to the email (or subscribing then replying)

Hey Fintech Nerds 👋

Welcome back! Hope you had a good break.

I went down the Crypto x AI rabbit hole and it’s fascinating. I’m rarely happier than when tinkering and learning.

This week I had to Rant about Stablecoins. Everyone selling them as cheaper is missing the point. I’m extremely bullish about Stablecoins, but not because they’re cheaper than card swipe fees.

Thanks to everyone for sharing your thoughts on The State of Fintech 2025.

Read on for why.

Here's this week's Brainfood in summary

📣 Rant: Stablecoins aren’t cheaper; they’re better

💸 4 Fintech Companies:

Auquan - Automating deep work in financial services.

Mural pay - The instant-cross-border network.

Ripe.finance The consumer and investment bank for the internet?

Dakota - Brex Built on Stablecoins?

👀 Things to Know:

📚 Good Read: Blackrocks Barbell

If your email client clips some of this newsletter click below to see the rest

Weekly Rant 📣

Stablecoins aren’t cheaper; they’re better.

I’ve seen countless think pieces claiming Stablecoins are a much cheaper payments rail comparing card interchange or SWIFT fees.

Stablecoins are not cheaper for most use cases yet. But they are better infrastructure.

We’re in the dial-up era of Stablecoins, so they’re still janky, and connecting is slow and painful (beep boop, bee boo beeeeeep).

In time, Stablecoins will create an abstraction layer above existing payment rails, just as the Internet did over the telcos. In the same way, entire sectors will become “onstable,” as we saw with video, messaging, and commerce. That network layer will eventually remove intermediaries and compete out costs.

But to get there, we need to understand where the cost of payments comes from. Spoiler alert: it’s not the networks like SWIFT or VISA; it’s the intermediaries, the risk they manage, and the incentive mechanism to drive adoption.

Previous efforts to compare costs confused network fees with the amount a merchant pays. So I put together this table to explain it.

For illustrative purposes only, your fee experience will vary

* The fee a direct member pays SWIFT is usually in pennies

* * Card network fees are an art form that is negotiated and will also vary wildly.

What makes Stablecoins unique is that they are programmable, global, and instant, making them a better choice for more transactions.

This drives bottom-up adoption from the global south.

The ability to access those markets will progressively increase industry adoption.

As that happens, we’ll stop needing to on-and-off-ramp because more and more activity will be done in a stablecoin native.

By the time that happens, intermediaries will create less value and the competition on price will intensify.

To understand the path there and who’s likely to succeed we have to understand

Why VISA itself isn’t actually expensive (infrastructure is)

Why SWIFT isn't actually expensive (risk is)

What Stablecoins actually solve (it's not risk - it's infrastructure)

Where the industry goes from here

VISA/MC aren’t expensive; intermediaries are.

Visa doesn't move money banks do.

Visa authorizes the movement of money.

Let's break down a $100 card payment:

Visa's actual fee: $0.15

Total merchant cost: $3.20

Where did the other $3.05 go?

Classic payments flow

In a $100 card purchase:

The merchant receives ~$96.80

The payment service provider (PSP) takes ~$0.85

The acquirer takes ~$0.10

Visa takes ~$0.15

The issuing bank takes ~$2.10 in interchange

Now think about

When your card gets stolen, who makes you whole?

When sanctions hit, who stops the payment?

When fraud happens, who takes the loss?

Every reconciliation, compliance check, and risk assessment occurs multiple times because each party needs to trust but verify.

And there’s a boat load of duplication:

The merchant's bank verifies the merchant

The card network verifies the transaction

The issuing bank verifies the cardholder

Each one maintains their own records

Each one manages their own risk

Each one needs to reconcile with others

That infrastructure cost compounds.

This is just for a simple card payment. The complexity compounds for international transfers via SWIFT: There are more parties, more checks, more reconciliation, and more risk.

This is why comparing Stablecoin fees to VISA or SWIFT fees misses the point entirely.

SWIFT isn’t expensive. Risk is.

SWIFT is not a payment system

SWIFT is a messaging system used by 11,000 banks in 200+ countries.

SWIFT doesn't move money; banks do. Money moves when a bank updates its accounts.

A simple cross-border flow - (Image from Matt Brown’s excellent blog)

Banks go through a series of messages to say who needs to get paid and for how much. Think of it like email.

Image from the excellent Matt’s Notes

“My customer wants to send you money.”

“Ok message received, please send the money”

“I’ve done my checks and updated my accounts”

“I’ve done my checks and updated my accounts”

A SWIFT payment message is not expensive. Depending on the message size, complexity, etc., it costs between $0.01 and $0.10. The cost comes from the bank fees for making and receiving those payments, which range from $40 to $120.

Cost comes from 1) Risk and Compliance, 2) Network complexity.

1. Risk and Compliance

The sheer amount of compliance and risk checks they have to do creates cost. A settlement can take 3 days to 3 weeks to complete via SWIFT. Some payments just get stuck and never happen.

Banks are "the police of money" - they must block transactions to sanctioned entities, manage currency restrictions etc.

Banks apply compliance by "knowing their customer" - easy for consumers, hard for complex company structures (e.g., owned by a holding company in Panama, owned by a trust company in the Cayman Islands)

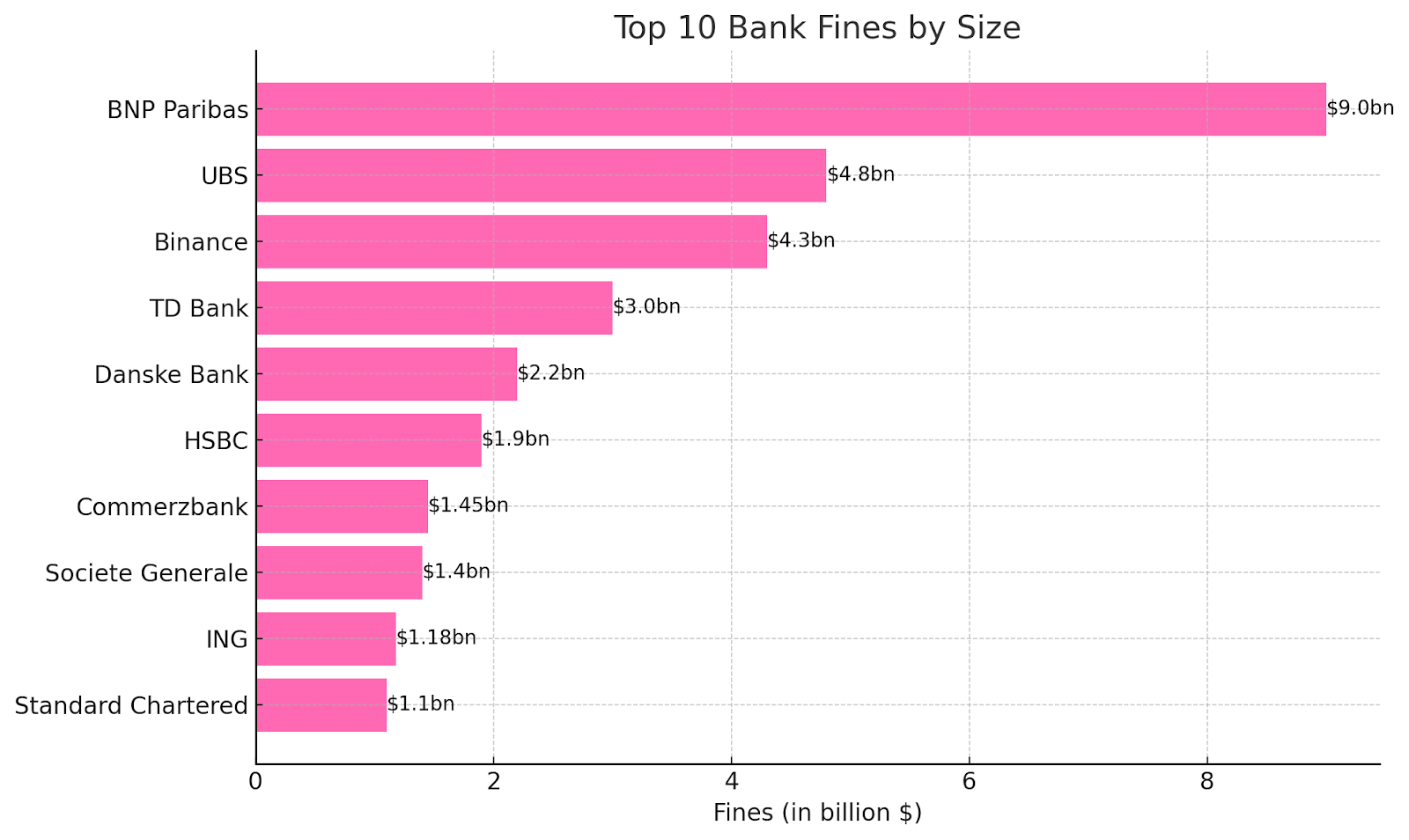

The cost of getting it wrong is massive: BNP Paribas was fined $8.9bn for sanctions failures, TD Bank $3bn.

2. Network Complexity

SWIFT is peer-to-peer but pre-dates the internet. We have DNS and TCP/IP with the internet that automatically route packets. SWIFT doesn't have this - every payment needs manual routing

Banks must build "correspondent banking relationships" - like getting married to another bank. This means understanding each bank, its jurisdiction, and how it manages compliance before they can transact with it. That all heaps on massive cost.

Depending on the bank, day, currency, and destination, a payment could take 100s of possible routes. This means your experience may vary, transfer times could be instant, take weeks or simply fail depending on routing.

One solution to this is to build a centralized entity like Western Union, which will always have limits to its network effects. SWIFT remains the ultimate backbone of finance because it is not centralized. If you want to get a payment to the absolute last mile, SWIFT is generally the ultimate fallback.

Just as the internet solved routing through protocols rather than bilateral relationships, Stablecoins solve payment routing through code rather than correspondent banking.

Stablecoins are financial infrastructure with new capabilities.

Like SWIFT messages, Stablecoin transactions themselves cost pennies.

However, the most important part is that the new infrastructure helps solve old problems.

1. Infrastructure

Stablecoins become a layer above existing rails. Just as the Internet protocol suite sits above telecommunications infrastructure, Stablecoins create a universal layer above banking infrastructure (like the Internet did above Telcos).

A single global record of transactions. 80% of the engineering and manual effort in finance goes into managing edge compliance-related edge cases and balancing payments against accounts. Stablecoins give you that record.

No more complex correspondent banking relationships. Large transactions will still carry risk and require compliance, but because it’s a single global network you can automate much of that.

In turn, this unlocks new capabilities.

Telecommunications (Voice over IP, streaming) and payments have become software. But like early VoIP, the value isn't in being cheaper—it's fundamentally different.

2. Capabilities

Available everywhere with an internet connection. Companies like Space X use Stablecoins to collect payments for Starlink as dollars. The USAID sends aid payments via Stablecoins.

A stable store of value. Consumers and small businesses can hold or transact with stablecoins in long-tail markets for stability and lower fees than using correspondent banking or money transmitters.

Global, instant treasury management for businesses. Think of Stablecoins like your checking account, and Treasuries as your savings account. Stablecoins plus money market funds make that global, instant, and 24/7.

Programmable automation (and compliance?). Want to bake rules into your payment? Stablecoins support that by default. It’s possible to build a token that would follow set rules.

People often miss the power of programmability. We’re already seeing Stablecoins launch, which has a native KYC requirement baked in. That is, you cannot receive a Stablecoin unless your wallet has been KYC’d.

That’s a very simple use case. Much more complex automation will be possible.

Stablecoins current state:

Are not expensive because the sticker price is only the network fee

This means today the compliance checks are as good as the wallets that initiate the payments

When those checks get added back in they will add costs not currently accounted for

However, the programmability and shared tate makes automating compliance the next big unlock for Stablecoins

Which over time will give Stablecoins a sustainable competitive advantage

But just like SWIFT, Stablecoins face the reality of risk.

The Power of Removing Intermediaries

Over time Stablecoins can become the technology that allows value transfer without requiring trusted intermediaries at every hop. This is profound.

The adoption pathway looks like this:

First, Stablecoins help reach previously underserved segments (like global south consumers and SMBs)

Then, they become the bridge between legacy payment rails

This drives a flywheel of on-chain activity

As more activity moves on-chain, the cost advantage of fewer intermediaries compounds

We've seen this pattern before with the internet. Email still often touches legacy systems but increasingly runs directly between servers. WhatsApp and iMessage bypass telecommunications entirely.

The same will happen with payments. Banks and processors won't disappear, but their role will shift from controlling infrastructure to providing value-added services on top.

This is why the infrastructure transformation matters more than current costs. Just as anyone can run their own email server (even if most don't), the ability to transfer value without intermediaries fundamentally changes the game.

Stablecoins will need to price risk

Wherever there are humans (or bots) transacting there is risk.

The financial industry does three things:

Store value

Move value

Price risk

Stablecoins do the first two in a very modern, global and automated way. But the risk pricing isn’t baked into the network fee.

You must account for risks like:

1. Operational Risk

Fraud and Compliance overhead. You can still be scammed, or have goods not show up from an e-commerce retailer. Using Stablecoins to evade sanctions or move money cross-borders without checks is still possible. What we do get is the programmability and observability of that new rail, which over time could structurally reduce cost.

The consumer protections (like chargebacks). The cost in consumer card payments comes from the protections (like getting paid back if you suffer from fraud). Those “fees” are an incentive structure for merchants and banks to refund consumers. Again could these be automated? What can we do with a single global record?

2. Financial Risk

Runs on Stablecoin issuers. The argument goes that “all funds are held in US Treasuries” so you don’t have to worry about an SVB situation. Not true. could see a “run on the Stablecoin issuer” just as we see a run on the bank. How do you know those treasuries have been bought? Who’s auditing them? What happens if there’s a major run? Expect this to mature.

Counterparty risk in settlement. Just because a Stablecoin transaction is "instant" doesn't mean the underlying settlement is. Someone still holds risk during that gap.

Wallet balance risk. Your Stablecoin balance in a wallet is only as good as that wallet's security and solvency. Just as FTX customers learned about exchange risk, wallet users will learn about wallet risk.

Bridge risk. Moving between Stablecoins or from Stablecoins to fiat often involves bridges or third parties. Each hop adds risk.

Real-time liquidity management. 24/7 markets sound great until you need to manage liquidity across them. Weekend volatility becomes a real concern.

Multi-currency complexity. Managing treasury across different Stablecoins (USDC, EURC) adds new dimensions to FX risk.

Yield optimization vs risk. The ability to instantly move between Stablecoins and yield products (like BlackRock's BUIDL) creates new opportunities and risks. Flash crashes or technical issues could trap liquidity at the worst moment.

The good news is we know a lot about pricing, the types of risk we see in cross-border payments, consumer cards, and B2B. Now we have a new technology to help us do that with a single global record of transactions.

This means Stablecoins won't be default cheaper, but they could be better.

All risk problems are data problems. If we can see the data, we can build a model for risk.

Stablecoins give us a single global record of transactions - the foundation for better risk management. That's why 2025 becomes interesting...

Stablecoins in 2025, More Regulation, More Banks, More Volume.

Today Stablecoins are tiny compared to any other form of rail, but when change comes, it comes quickly.

The US dollar has the greatest product market fit of any product in history. Argentina is looking to dollarize. The adoption of Stablecoins today is bottom-up and outside local regulatory systems. It’s not always pretty, but it is inevitable.

Here’s how I think 2025 plays out.

Every PSP does Stablecoins: With Stripe acquiring Bridge, what will Adyen and PayPal do? PayPal has PYUSD and lots of pieces, but they don’t integrate. Adyen, with its more enterprise focus, isn’t being dragged there but watch companies like Nuvei, DLocal, and especially Onafriq. Companies like BoomFi* help PSPs whitelabel stablecoin capability.

Regulation is the unlock for institutions. The EU's MiCA regulation, US state frameworks, and Singapore's progressive stance aren't stopping Stablecoins - they're legitimizing them.

CBDCs won't replace Stablecoins - they'll likely power them. Just as the internet didn't replace telecommunications infrastructure but built on top of it, CBDCs will probably become part of the Stablecoin ecosystem rather than a replacement for it.

In 2025 every bank needs a Stablecoin strategy: In 2024 Societe Generale became the first bank in the world to issue a Stablecoin, in 2025, companies like Brale are making this possible for any bank.

In 2025 tech-forward global corporates will adopt Stablecoins: If Brex made Stablecoins a feature, instantly, their client base would have access to many more markets. They could also potentially manage 24/7 swaps for money market funds.

We start to see Stablecoins as a layer above payments infrastructure. Just as the internet sits on top of the domestic telco networks, Stablecoins will start to sit on top of domestic payment methods and rails. We can still use SMS, but iMessage and WhatsApp are much more popular.

The rise of local Stablecoins and Fiat off-ramps. The big bottleneck in Stablecoins today is local currency liquidity. Expect this to change rapidly in 2025.

Stablecoins as Money for the Internet

Traditional rails won't disappear, but they'll become utilities underneath a Stablecoin layer. Just as over-the-air TV, FM radio, and SMS still exist, but they’re not where the future of telco is. The winners will not be those who saw Stablecoins as cheaper rail but as the foundation of a new financial stack.

Who Wins, Who Loses?

Winners:

Tech-forward banks that move early (like Société Générale)

Payment companies that bridge old and new (think Stripe)

Treasury teams at global companies (think SpaceX)

The Challenged:

Traditional correspondent banks dragging their feet

Legacy payment processors not willing to try

Banks betting on closed systems

Those thinking long-term are making the 10 and 20-year bet that Stablecoins or something like them are inevitable.

The future isn't about cheaper payments. It's about better ones.

The payments industry leaders of 2035 reorganized around Stablecoins, tokens, and an internet-native financial system.

It’s how, not if.

ST.

4 Fintech Companies 💸

1. Auquan - Automating deep work in financial services.

Aquan provides AI tuned for finance use cases like creating credit or investment committee memos, or new deal screening. It notes clients like Met Life, UBS and a top 10 asset manager using the product in production, taking tasks from 20 hours down to 5 or 10 minutes.

🧠 The battleground for app-level AI is performance quality. This quote on the homepage stood out “This is the first time I’ve seen this work.” So often the AI agents promise the earth but don’t quite stick the landing. Your brand is your consistency, your consistency is your brand. This is even more true in the age of AI-generated slop.

2. Mural pay - The instant-cross-border network.

Mural pay aims to help companies with cross-border payouts, virtual accounts, invoicing and currency conversion in 170 countries and 40 currencies. Crucially they ”guarantee delivery” and offer instant settlement. Mural Pay offers all of this through a single API.

🧠 Wise is that you? It’s unclear if they’re using Stablecoins (I couldn’t find a reference), but if they are, the value will move. But if they are, then this literally looks like someone connected the Wise infrastructure API to a Stablecoin. The “guaranteed delivery” sounds crazy for payments but in cross-border, especially for the global south payments fail anywhere between 5 and 20% of cases (depending on where you live and what you do).

3. Ripe.finance The consumer and investment bank for the internet?

Ripe offers simple deposits and loan products for Crypto natives on top of a more complex investment bank-like structure. Users can deposit Stablecoins and earn yield, borrow against their collateral (a single loan against multiple assets which makes them unique).

🧠 This is DeFi at the back, banking at the front but with a consumer grade UI. Ripe is odd. When you strip this back, it’s DeFi but repositioned simply, and that’s actually genius. It takes deposits, gives loans, issues bonds, and runs an endowment fund. Like everything in DeFi it’s wrapped in the sectors jargon, but… I think they’re on to something with this positioning. What makes DeFi so confusing is the entire back office of a bank is essentially community run and covered in the whitepaper. I low key just want a professional team to run this thing like a bank but use DeFi rails. Decentralized governance is a nice ideal, but the practical reality is a handful of people run a protocol with a gallery of bag holders watching the drama unfold blow by blow. Transparency is good, we should keep it, but we shouldn’t confuse it for control.

4. Dakota - The Stablecoin account for SMBs

Dakota is a Stablecoin equivalent to a Wise multi currency wallet in some senses. Users can accept and send USD or EUR, store deposits as Stablecoins (treasuries) and earn up to 4% yield, and spend management cards. The service also has a smart router that’s designed to help payments get to their destination as fast and cheaply as possible. They also advertise 24/7 money movement with Stablecoins.

🧠 What’s caught everyone’s attention is the idea that vs. a bank account this is smarter and SAFER(??!). The argument goes that because Stablecoins are issued against US Treasuries held at a custodian, there is zero risk of a bank run (SVB scenario), because US Treasuries are government backed. But as many have pointed out, who’s issuing the Stablecoins? What’s their risk? What happens if they fail to make good accounts as an intermediary? Stablecoins are not safer because US treasuries. They could be if properly managed but the word “if” is doing a heavy lift in that sentence. What’s sad is using Stablecoins for multi currency accounts will eventually become a default, and this seems like a strong team. Just a rookie move in the marketing. There is a truism in the techthat Stablecoins are safer because treasuries. Let’s put that one to bed shall we?

Things to know 👀

The top banking regulator from the Federal Reserve will step down on Feb 28th after speculation the Trump administration would look to replace his role. He will stay on the Federal Reserve Board. Bank stocks rallied more than 1% in the wake of the news.

🧠 The most obvious implication is for Basel III. Barr was a key proponent of the regulation. Potential candidates, such as Governor Michelle Bowman, have previously supported less stringent regulations. Basel III could face delays, modifications, or even potential rollback, depending on the regulatory philosophy of the new appointee and the administration's broader approach to financial regulation.

🧠 The “Novel activities” and Crypto industries have almost a clean sweep. Expect to see much more activity in embedded finance, banks getting into Stablecoins and trying again with how they support Crypto businesses (especially as we enter a new bull market).

🧠 Pausing activity while regulators look for a needle in a haystack created a freeze. The material complaint in so-called “Operation Chokepoint 2.0” is that persistent and vague regulatory letters from the FDIC left banks unable to operate or open new programs. This effectively “choked” their business while regulators looked for risks they didn’t necessarily understand.

🧠 Two things are true: Regulators were right to look, but they also “choked” business. We saw big Crypto blow-ups, and some operational risks in Banking as a Service have harmed consumers. They didn’t know at the outset how they’d find those risks. Yet in being vague, and looking everywhere, multiple times, it became impossible to do business.

🧠 Not everything is high-risk, and there are plenty of good actors in Crypto and Embedded Finance. The “Hey everyone, can you just stop doing business while we take 4 years to take a look” approach hasn’t worked and created a huge backlash from the private sector. It united banks, fintech companies, and crypto companies against the US Government.

🧠 The alternative shouldn’t be a caveat emptor approach to financial products. We need consumer protections, but we can’t shut entire sectors of the economy while we figure those out. We need a step-change of innovation and automation in supervision.

Revolut is developing a private banking service for high-net-worth individuals (HNWIs), typically defined as people who hold liquid assets of over $1m, according to three job listings on its website. They’re hiring relationship managers, compliance and legal staff with expertise.

🧠 Revolut is attacking the profit centers of banking. Neobanks and digital banks used to be easy to ignore, but if you’re a European bank CEO, Revolut is now coming for your profitable customer base.

🧠 Revolut’s has figured out compliance + blitzscaling. Blitzscaling is the art of doing 100s of things as MVPs and doubling down on products that work. In an interview in December, the CEO said they have at least 10 new products in development at any one time, of which 5 might succeed.

🧠 Small bets, big outcomes. The 10 new product bets might have teams of 6 to 12 working on them, and be quickly killed if they don’t hit KPIs. Contrast that with a bank and annual funding cycles and internal program management structures. It’s wildly different.

Good Reads 📚

Active managers like Pimco and Schroders are losing favor. Despite delivering impressive performance, the market doesn’t want to pay higher fees for supposedly market-beating performance. In 2009 came the passive (ETF) wave which Blackrock got into with the acquisition of Barclays Global Investors..Now it’s moving back to higher margin segments infrastructure and recently, private credit. What Huw Van Steenis called Blackrock’s barbell strategy.

🧠 Blackrock has a knack of re-inventing itself in time to catch the next wave. Today “alternatives” like Infrastructure and Private Credit are just 4% of revenue but nearly a quarter of earnings.

🧠 Never let a good crisis go to waste. Blackrock’s early acquisitions in 2004 became tests for how to integrate a company. Gradually going bigger, and going deeper into the new thing.

🧠 The secret weapon is their Aladdin core system (built by friend of the newsletter Scott Codron, h/t to you sir). It’s flexible enough to provide risk management for clients and Blackrock themselves.

🧠 The mergers are always designed to create diversification not cost cutting. Aladdin helps them get operational synergy sure, but the real benefit is that they can make life easier for clients with the “single global platform.”

Tweets of the week 🕊

That's all, folks. 👋

Remember, if you're enjoying this content, please do tell all your fintech friends to check it out and hit the subscribe button :)

(1) All content and views expressed here are the authors' personal opinions and do not reflect the views of any of their employers or employees.

(2) All companies or assets mentioned by the author in which the author has a personal and/or financial interest are denoted with a *. None of the above constitutes investment advice, and you should seek independent advice before making any investment decisions.

(3) Any companies mentioned are top of mind and used for illustrative purposes only.

(4) A team of researchers has not rigorously fact-checked this. Please don't take it as gospel—strong opinions weakly held

(5) Citations may be missing, and I’ve done my best to cite, but I will always aim to update and correct the live version where possible. If I cited you and got the referencing wrong, please reach out