Welcome to Fintech Brainfood, the weekly deep dive into Fintech news, events, and analysis. You can subscribe by hitting the button below, and you can get in touch by hitting reply to the email (or subscribing then replying)

Hey Fintech Nerds 👋

Was this the biggest week ever in Fintech?

Two mega-stories. Chime had their IPO, Stripe made their second massive stablecoin-related acquisition (Covered in Things to Know 👀)

In any other week, I’d have covered: Klarna launched a debit card, Coinbase launched a co-branded Amex card, with 4% back on Bitcoin, business accounts on stablecoins, Shopify is accepting USDC, the GENIUS Act heading to a final vote, Ant Group doing stablecoins, and the FCA partnering with Nvidia. Each of these stories is rant-worthy.

The picture emerging from all of this is that Fintech is caught between two dueling weather systems. AI and stablecoins. A lot of it is hype, and a lot of it will fade; the IPOs may come down before they find their long-term value.

And when that happens, don’t lose focus.

Because there is a genuine shift in the platform of finance, the system of record, and the infrastructure.

Here's this week's Brainfood in summary

📣 Rant: Stablecoins are a platform pt - OnChain FX is the gateway drug

💸 4 Fintech Companies:

👀 Things to Know:

Gmail users: You’re missing most of the newsletter - Click “Read Online” below so you don’t miss out on my take on Stripe’s new acquisition.

Weekly Rant 📣

Stablecoins are a platform pt 2 - On Chain FX is the Gateway

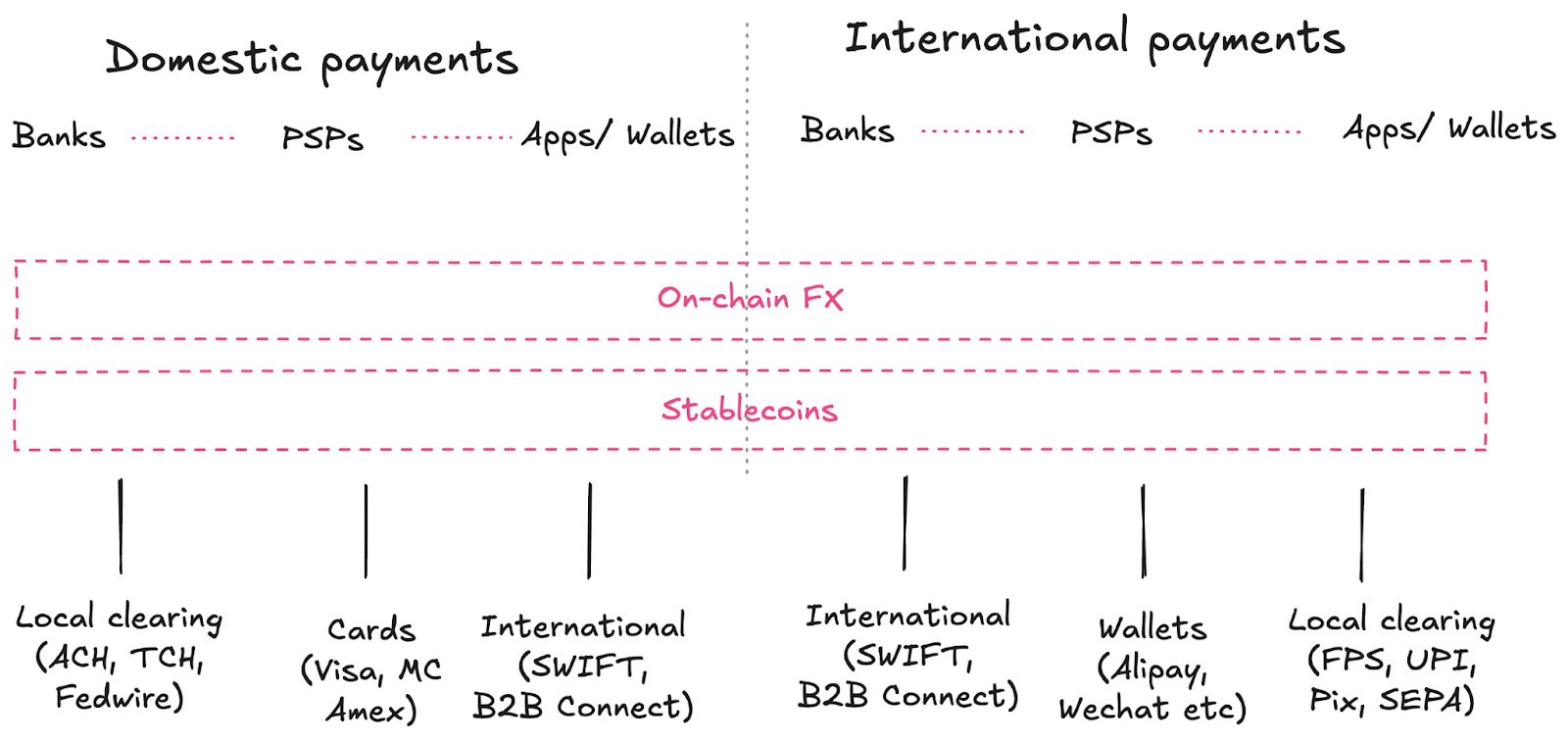

Stablecoins are about to collapse the distinction between FX and payments.

When both dollars and Brazilian reals live on-chain, corporate treasury transforms from "USDC → off-ramp → BRL" to simply "USDC → BRL." No correspondent banks. No pre-funding. No settlement lag.

Jack Zhang from Airwallex thought stablecoins were over hyped.

His tweet crystallizes the sophisticated skeptic position: stablecoins are just another exotic rail, not meaningfully cheaper than Wise or JP Morgan Kinexys in G10 currencies.

He's right about today's economics. But he's missing the phase transition that shifts the economics entirely.

Stablecoins are about to fundamentally rewire cross-border. Not because they're cheaper than SWIFT - they're not yet. But because they're about to combine FX and payments into a single transaction. No pre-funding, less middlemen, less fees.

And if we can combine FX and settlement, imagine what else we can do.

Today

The current market reality, “A useful rail for exotics”

The reality of treasury and FX at scale

The criticism against stablecoins as a long-term platform shift

Why the market will continue to evolve

Regulatory clarity is coming

On-chain FX changes the economics

On-chain finance changes treasury

And you need a stablecoin strategy that accounts for tomorrow not just today

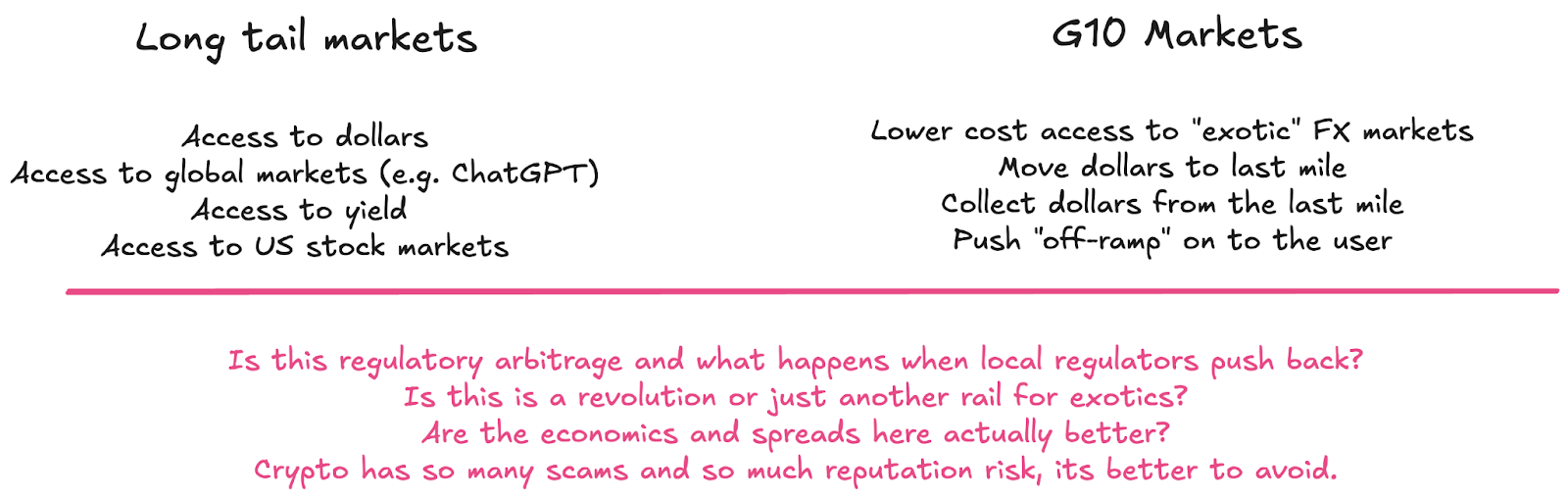

The mainstream view: “A useful rail for exotics”

If I’ve understood correctly, Jack views the world like this:

The market picture today?

I’ve recounted the use cases before but here’s a quick summary

Consumer: Holding dollars in countries where the local currency isn’t stable

Consumer: Spending dollars with stablecoin linked cards (instead of using an account)

Business: Payroll in dollars at lower cost avoiding local banks (e.g. Deel)

Business: Collections in dollars without dealing with local banks (e.g. Space X)

Business: Global financial accounts (e.g. Stripe financial accounts in 120 markets)

Many of these use cases push the on-off ramp problem to the last mile or avoid it entirely. For these businesses, living in dollars is the product.

To understand how we go beyond this, we need to understand the how banks, money movers, and corporates think about cash, treasury and FX (in the G10 and exotics).

The reality of FX and Treasury at Scale

If you’re running 100s of billions of cash per day, tiny details matter, especially.

Liquidity. Do I have the right cash, in the right place, with the right bank, in the right currency?

Risk. Are currency moves, interest rates, debt rates, bond rates changing and does that impact my liquidity?

Teams ask these questions daily, quarterly, annually, and become the nerve center for reporting. If it breaks, the company breaks. It’s beyond mission-critical not to mess this up.

These companies and treasury teams are highly sought after by money center banks, who want to sell them deposits, payments, FX, supply chain financing, and a whole suite of products.

For a Space X or Uber, they’re more tech forward, stablecoins are something they can adopt (and will get banks attention, because they’re unicorn client wins for a Global Cash Management team).

A traditional, large global corporate will typically have relationships with 10+ banks and maybe a handful of local banks, depending on their needs. Their system of record is the ERP (e.g,. Oracle, SAP, Microsoft Dynamics).

So if they’re so conservative and so well served by banks, why would they look at stablecoins?

The Criticisms of Stablecoins as a long-term option

There are four big critiques Jack made, and that I hear often.

Regulatory arbitrage will create pushback from nation states. China recently issued an outright ban on crypto. The Chinese payments world view of stablecoins had been most people using stables locally were bad actors, fraudsters etc.

The dollar use case is only valuable for exotics. Smaller markets are often not well penetrated by banks, and SWIFT payments can be slow or expensive. “Useful but not a game changer?”

The unit economics aren’t cheaper. With large banks and modern solutions like JP Morgan Kinexsys, companies like Airwallex or Wise already have instant, 24/7 settlement at tiny spreads from spot (e.g. 30bps) to most global markets.

“It's crypto” - Lest we forget, FTX, the ICO scams of 2017, and the dark net drug markets

These are valid concerns.

And if this world view were true, stablecoins are still an incredibly valuable use of time, opening up many (not all) global markets that were previously expensive. But that’s not why Stripe acquired Bridge (and then Privvy this week), or why global banks are taking this much more seriously than I’ve ever seen (in 2017, 2021 or any time since).

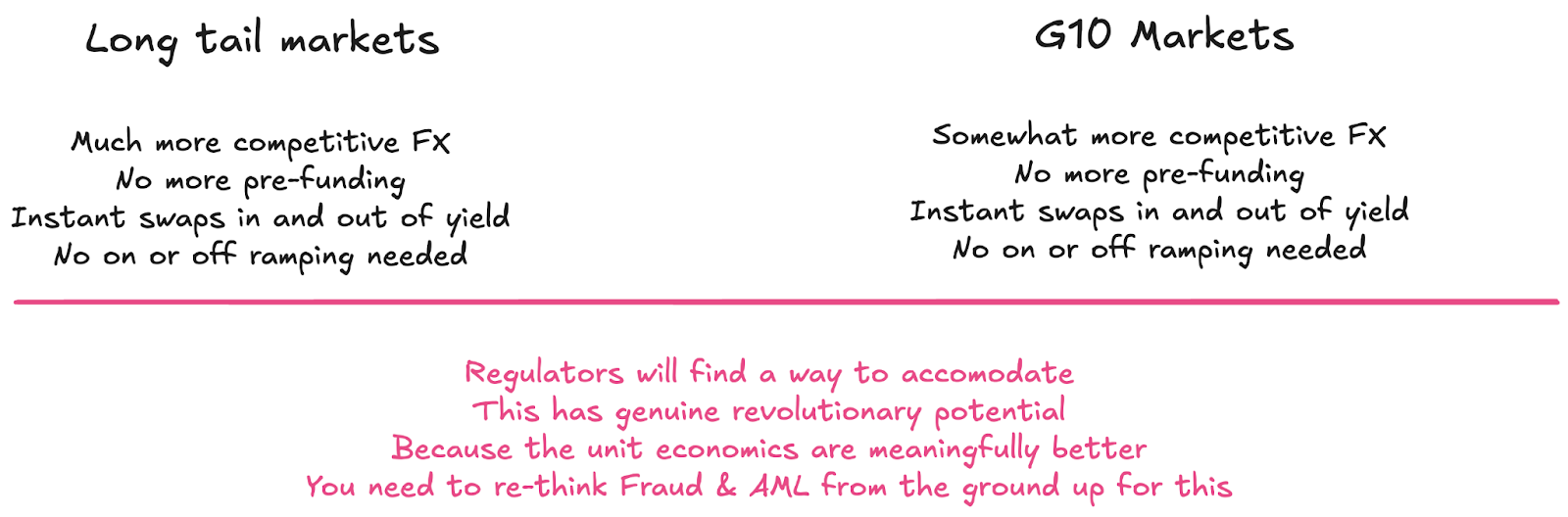

The market will continue to evolve from where we are today

The world will look very different in the next 12 to 24 months. Each of Jack's concerns has a straightforward response:

Concern today | Reality tomorrow |

Regulators will shut this down | The GENIUS Act is a game changer on shore. Exotic markets will accommodate as Fortune 500’s adopt |

Not cheaper than existing rails | On-chain FX eliminates the cost structure |

Not useful for G10 currencies | Combining FX, Money Markets and Settlement is a game changer for treasury |

It's crypto/reputationally risky | The reputation is shifting. But you have. to get compliance right from day 1. |

The timeline matters here if you’re a business making investments and decisions. This pattern is coming, but the market is still early.

So I’d amend my picture from earlier to look like this:

A new market reality is coming in 12 to 24 months

Regulatory clarity is a step closer

This week, the GENIUS Act progressed another step towards its final vote. As that happens, major institutions like Bank of America are talking up their intention to enter the market. Institutional legitimacy is now a matter of time. The Bank of America CEO is telling the market they’re looking at it.

Therefore, I think it’s more likely regulators try to accommodate this reality than fight it. Yes, China instigated another ban on Crypto, but in the same week, Alibaba is applying for stablecoin licences in Hong Kong.

On Chain FX disrupts the cost structure.

When both dollars and local currencies are on-chain, FX becomes instant.

Today, to move money between the USA and Brazil, a money mover like Wise or Airwallex has to store millions at local banks to cover any needs. With stablecoins and on-chain FX, that becomes instant and 24/7.

For these companies, there is a marginal benefit in adopting stablecoins, allowing them to access more users and better foreign exchange rates in non-G10 currencies.

The reality of “instant” 24/7 payments today isn’t actually instant; it’s pre-funded. That pre-funding can be expensive. When banks accept, clear, and settle stablecoins directly in local currencies, everything changes from this:

Dollars → on ramp → USDC → off ramp → local fiat (e.g. BRL)

To this:

USDC → BRZ.

No on-ramp, no off-ramp means a more seamless experience for users, sure. But more importantly, it eliminates the capital requirements that drive up costs.

This changes the economics of cross-border in two ways.

Stablecoins remove the need for cash pre-funding. If a local bank clears and settles stablecoins, you don’t need to leave 10s of millions of dollars there to cover your liquidity needs.

Combining On Chain FX and settlement changes the unit economics. That pre-funding creates credit risk, liquidity risk which shows up in pricing. The gap between FX markets and SWIFT payments are where all the friction, slowness and therefore cost is.

The shift to the $7.5 trillion daily FX payments market happens when:

Corporate Treasury teams don’t need to pre-fund accounts.

FX rates come down to near spot instead of +30/60bps

Banks in Brazil can transact with Singapore without going through 4 or 5 correspondent banks (adding cost and slowness)

In G10s, where we have instant settlement and direct correspondents, the on-chain market can attack the already tight margins of incumbents

The practical matter is that today liquidity is fragmented, and in many routes FX is still cheaper and better via traditional rails.

But this is changing rapidly.

Conduit* is enabling liquidity via on-chain swaps

Stablesea is aggregating liquidity as a service

OpenFX is building deep liquidity itself.

In Brazil, Braza Group is a bank that has issued a stablecoin specifically for on-chain FX. Suddenly, the business case for banks, corporate treasury teams, and anyone moving money just got a lot more interesting.

A couple of weeks ago I said stablecoins are a platform. Now we’re starting to build things on that platform.

On-chain FX is coming

On-Chain FX is only just arriving. But now that banks have arrived, it will scale quickly. Then we can start to tokenize other assets.

On-Chain FX vs Pre-funding

When Wise or Airwallex advertises "instant" transfers to Brazil, they're not actually instant. They're pre-funded. Understanding this distinction is crucial to grasping why on-chain FX represents a phase transition, not just optimization.

Napkin version of how pre-funding works

For a $100M annual corridor (e.g. Brazil), this means:

$8-25M in Brazilian banks as overdrafts (and fees)

3-5% annual funding cost = $240K-1.25M yearly

Operational complexity of managing 50+ bank relationships

Regulatory capital requirements in each jurisdiction

Now lets take a $1m payment and break that into real numbers in pre-funding:

Base FX spread: 40-60 bps = $4,000-6,000

Pre-funding cost allocation: 7.5-12.5 bps = $750-1,250

Correspondent banking fees: 10 bps = $1,000

Operational risk buffer:10 bps = $1,000

Regulatory compliance: 5 bps = $500

Total cost: 70-100 bps = (or $7,250-9,750.)

On Chain FX not only eliminates pre-funding, it can eliminate correspondents and some of their fees. In this world, FX is automated with “automated market makers” (AMMs). Using current DeFi economics as a baseline* the breakdown looks like this for a $1m payment:

DEX/AMM spread: 5-15 bps = $500-1,500

Network fees: 0.2 bps = $20

No pre-funding required: 0 bps = $0

Compliance cost: 5 bps = $500

That puts a total cost closer to 10.2-20.2 bps = $1,020-2,020 for a cost reduction of 85-90%. This only works once liquidity arrives and the infrastructure matures. But that race has started.

* Note - current DeFi economics didn’t account for compliance, I added that back in at full price, but it could come down.

As more currencies go on-chain, the efficiency gains compound exponentially:

2 currencies: 1 trading pair

5 currencies: 10 possible trading pairs

10 currencies: 45 possible trading pairs

20 currencies: 190 possible trading pairs

In the traditional model, each pair requires separate infrastructure. On-chain, each new currency automatically creates trading pairs with every existing currency.

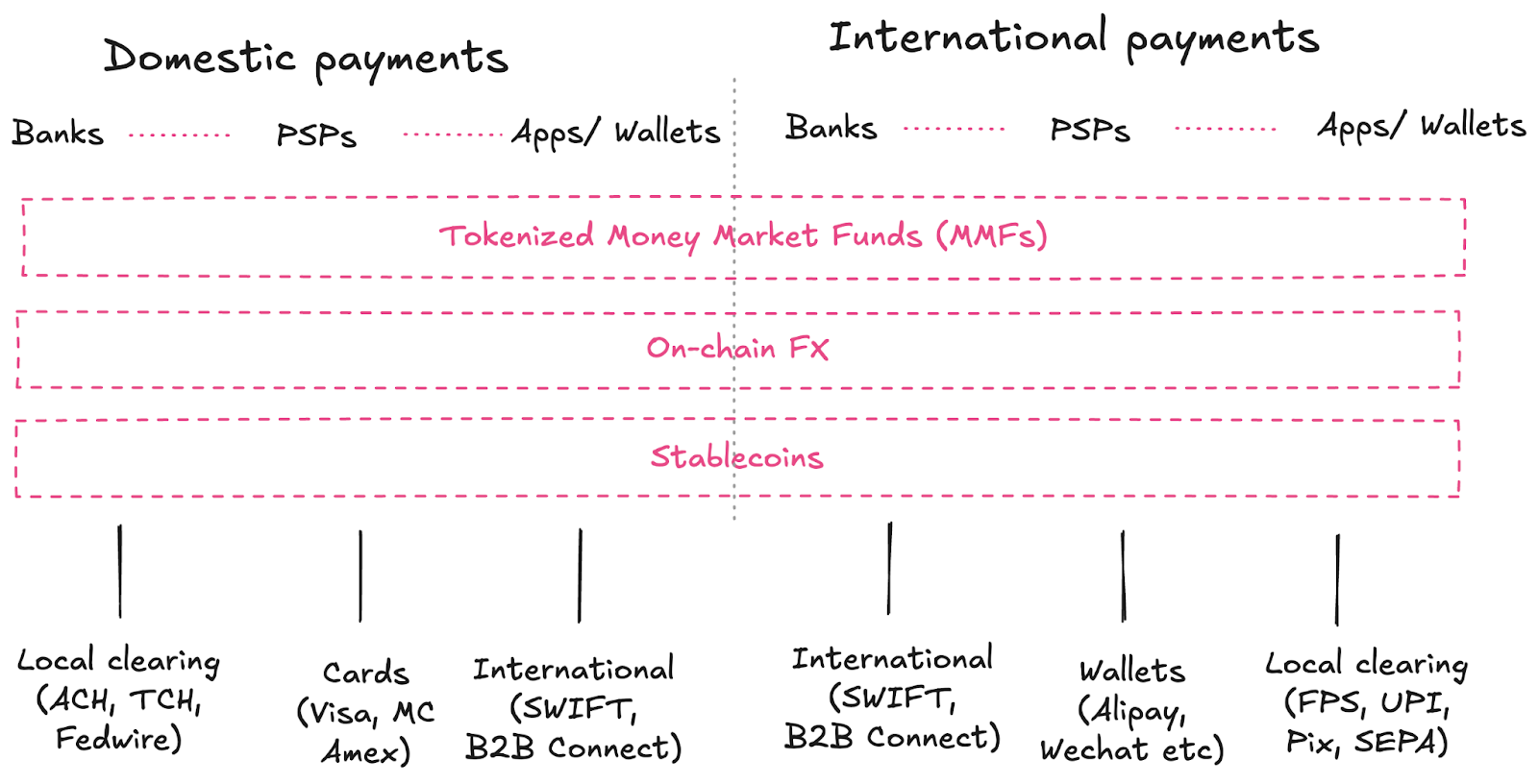

But on-chain FX is just the beginning. When corporate treasury goes fully on-chain, the entire waterfall changes:

Stablecoins become a platform for treasury managers.

Think about the treasury management waterfall today.

Hold n days of working capital at banks

Hold n+n days of capital in Money Market Funds (MMFs)

Store longer-term capital in yielding assets

Now, when the corporation in Brazil has to pay a supplier in Singapore, they have to sell a money market fund (which could take 24 hours, or longer on a weekend), then start a SWIFT payment.

With stablecoins, it looks like

Hold n days of working capital in stablecoins

Hold n+n days in tokenized MMFs

Store longer term capital in tokenized securities, bonds etc.

To pay a supplier in Brazil, they could instantly swap the tokenized MMF for a stablecoin, then swap the BRL stablecoin for SGD. This avoids the delays in selling treasuries, operates 24/7 and becomes a genuine alternative to the correspondent banking system.

On chain finance - the revolution will be tokenized

If that sounds far-fetched, remember, this is how on-chain finance has been working for several years now, transacting 10s of billions, it just was crypto native treasuries and using crypto exchanges.

It’s about to get a lot more mainstream. For example, I saw Kybria has an integration with Fipto to give teams access to stablecoins.

The sleepy backwater that was corporate treasury management and ERP systems is getting interesting.

Fraud and Money laundering need a new approach

There will be fraud & money laundering, but we won’t fix it the old way.

One question I get often is “what’s the actual scale of Fin Crime risk in stablecoins” - and based on every study I can see, it’s at worst about the same as the existing system, and at best, 10x lower.

In the existing system a sanctions hit, or a transaction monitoring alert can trigger an investigation where an analyst has to chase a paper trail back through 3 or 4 correspondent banks.

When you have a golden source of every transaction ever (on a blockchain), your fincrime investigations become very different. Every money mover needs to get comfortable with wallet screening and operating with “self-hosted” wallets as being digital cash.

With stablecoins, we have a golden source of transactions (the blockchain), and we can use messaging services (like IVMS101) to securely communicate with other payments companies or wallets to investigate financial crime.

This new world needs new tools, systems and processes that can manage risk in both worlds.

Everyone needs a stablecoin strategy

You can come a long way in a week of paying attention to stablecoins.

Once you recognize the opportunity, the next question is, what can you practically do?

You need:

To understand your revenue opportunities. I recently did a podcast called "The 8 Ways banks can make money from stablecoins." This is a good starting point. Treasurers, money movers, your value will be in the bps and compliance automation.

Much more institutional knowledge on stablecoin regulation. I can introduce you to the team at Global Digital Finance, the nonprofit I founded that can help.

A working knowledge of the mint/burn audit trail. How treasuries or repos custodied at say BNY, brokered by Blackrock, become tokens minted by Circle, brokered by market makers like DRW, and custodied at Fireblocks or Anchorage.

If you were to bank the sector, how would you provide an audit trail from your systems of record all the way through to the blockchain?

If you were to bank the sector, or support corporate treasury teams in accessing stablecoins you'd need new AML tools and ops processes. Batch transaction monitoring won't cut it for real-time, 24/7 and global. At Sardine, helping companies manage on-chain and off-chain compliance is our specialty.

The correspondent banking system took decades to build and centuries to optimize. On-chain FX can replicate that optimization in far less time because it's composable infrastructure, not bilateral relationships.

Jack's framework assumes stablecoins have to compete within existing market structure. But they're building a new market structure entirely. One where FX, payments, and yield are all part of the same instant, global, 24/7 system

Want to take advantage? You have work to do

Figure out the flow of funds. Figure out the edge cases. Figure out your risk appetite as regulation shifts.

That sounds like fun to me.

ST.

4 Fintech Companies 💸

1. Rizon - The stablecoin-linked card for LATAM

Rizon is an app that helps users hold, send or spend stablecoins. Users can deposit Tether or Circle and then spend that balance anywhere Visa is accepted. The app is “self-custodial” (meaning the user holds the balance), but unlike cash, it can be used to pay for global products like Netflix, Airbnb, Uber, etc.

🧠 The “off-ramp” is dead. Stablecoin-linked cards are a better solution for users in the global south who want to hold dollars and spend directly from that balance. Being cash-like, they avoid a lot of the challenges with traditional prepaid cards which can be complex and expensive to operate. With Google and Apple Pay, the cost of distributing these cards goes to 0. Why wouldn’t every company with remote workers (like say, Uber) do something similar?

2. Shuffle - The App that rewards dining out.

Shuffle users get 10 to 100% off their bill every time they dine out at a participating restaurant. They work with independent spots to bring them new customers. Users connect via open banking and get automatically rewarded once they have spent at a participating location.

🧠 This feels like a feature for food delivery apps. Restaurants already make extra cash from the deliveries from companies like DoorDash or Uber Eats, but imagine if there was some sort of incentive to drive in-location dining too. Instacard does things like 2% cash back, and they have an ads business, but shuffle neatly connects those. The UK apps like Deliveroo or Just Eat could do well by partnering.

3. AIbidia - The Transfer Pricing AI

Aibidia helps multinational corporations manage “transfer pricing,” where one legal entity in a group pays another (sometimes nicknamed wooden dollars). The platform connects all ERPs and sources of truth to manage transfer pricing reporting, compliance and help build accurate segmented P&Ls

🧠This is the classic “office of the CFO” problem nobody knows until they’ve lived it. Imagine your HQ in London has a central tech team that serves 100s of countries. Each of those countries pay for the work they got done, and all of that is added up, accounted for, often manually or in an old ERP. This was aching for innovation.

4. Froots - Active fund management for Europe

Froots is a digital-first investment manager that provides exposure to actively managed funds. They invest in ETFs, ETCs and bonds, then dynamically managed based on a users goal (e.g., liquidity optimization or long term wealth building)

🧠Active management has lost favor in HNW, but is coming down market. 10 years ago, “alpha” in active management firms was all the rage. With the rise of ETFs and private markets, and permanent capital vehicles, it has become less popular with ultra-high net worth and family offices. Perhaps a new segment and a new market (Austria) is a better play?

Things to know 👀

Chime just priced their IPO at $27 per share. $7.2 billion valuation. 30 mins from open stock was up nearly 60% to $44. Chime is the Neobank that serves people making under $100k. A recap of their S1 numbers, 67% use Chime as their primary bank, $121B in annual purchase volume, 88% gross margins, 54 transactions per customer per month

🧠A new business model. Chime is the poster child for US Fintech (perhaps unfairly), but they’re actually to my mind, the poster child for a new kind of customer and a new business model to serve them.

🧠 The Durbin Ammendment created a Fintech Opportunity The Durbin Amendment was supposed to help community banks compete with JPMorgan by letting smaller banks charge higher interchange fees (44¢ vs 21¢ per swipe).

🧠 Community banks couldn't scale this advantage. Chime could. The regulation designed to help Main Street banks accidentally created the infrastructure for Silicon Valley fintech. By partnering, Chime was able to use the extra 23 centrs per transaction for free checking, no minimums, no fees.

🧠 Chime is serving the 75% of Americans earn under $100k. Their average is $30k (but moving up). The traditional solution: charge fees to offset serving costs. Instead of charging customers to cover costs, they made customer activity inherently profitable. Every debit swipe generates revenue. More usage equals more profit.

🧠 Chime makes money from interchange. Customer spending equals revenue. They literally cannot profit unless customers are spending money they actually have. That incentive alignment creates trust, and you’d imagine, the opportunity to cross-sell.

🧠 Will a republican administration close this Durbin gap? If Congress decides this regulatory arbitrage has gone too far (and it kind of is arbitrage), the model breaks.

🧠 Chime is gonna do Chime. They take their time and are always ultra-aggressive on customer centricity and fees. Compared to global “comps” like Revolut or Nubank, Chime is incredibly low-cost and low-ARPU

🧠 Their moat isn't technology. It's trust from a demographic that's been burned by traditional banking for decades. Lose that trust chasing growth, and the whole thing unravels.

🧠 They have “no plans for a charter.” “Uber doesn’t need to own the cars to be better” - if anything a charter is something they see as a distraction.

🧠 They see more upside from their existing TAM. Their average customer income is $30k, there’s a lot of room in the sub $100k to win new clients. Conventional wisdom suggests that you should target $200k+ customers. They see the non-affluent segment increasing in size.

🧠The cash can help but wasn’t needed. They have space for opportunistic M&A (and stock as another lever). So if you were Chime, what would you buy?

Stripe just made their second major crypto acquisition. After spending $1.1bn on Bridge, they just bought Privy for an undisclosed sum rumoured to be mid 9 figures. Privy is a developer-focussed wallet infrastructure company, it helps handle the complexity of creating and managing “wallets” for on-chain finance and other use cases.

🧠 The strategy: Become the developer choice for on-chain everything.

Bridge ($1.1bn) = Stablecoin Infrastructure Stripe can now process stablecoin payments like any other transaction.

Privy (just acquired) = Wallet-as-a-Service Makes wallet creation, balance management, and transaction signing as simple as an API call.

🧠 How they work in combination: Bridge handles the stablecoin rails, Privy handles the wallet complexity and Stripe keeps its reputation for simplifying complexity for developers

🧠What this enables:

Any marketplace can offer crypto wallets to users

Any fintech can add stablecoin accounts

Any platform can settle globally in seconds

All through APIs developers already trust.

🧠The future is self-custodial: We’re moving from a world of accounts to one where wallets enable companies to create “account-like” experiences without the traditional infrastructure.

Think about that for a second.

Tweets of the Week

That's all, folks. 👋

Remember, if you're enjoying this content, please do tell all your fintech friends to check it out and hit the subscribe button :)

Want more? I also run the Tokenized podcast and newsletter.

(1) All content and views expressed here are the authors' personal opinions and do not reflect the views of any of their employers or employees.

(2) All companies or assets mentioned by the author in which the author has a personal and/or financial interest are denoted with a *. None of the above constitutes investment advice, and you should seek independent advice before making any investment decisions.

(3) Any companies mentioned are top of mind and used for illustrative purposes only.

(4) A team of researchers has not rigorously fact-checked this. Please don't take it as gospel—strong opinions weakly held

(5) Citations may be missing, and I’ve done my best to cite, but I will always aim to update and correct the live version where possible. If I cited you and got the referencing wrong, please reach out