Welcome to Fintech Brainfood, the weekly deep dive into Fintech news, events, and analysis. You can subscribe by hitting the button below, and you can get in touch by hitting reply to the email (or subscribing then replying)

Hey Fintech Nerds 👋

This week the DoJ alleged Visa has a monopoly because it does capitalism. Get this; it offers bulk discounts and incentives to its partners. WILD right? 🙄

Chime is planning to IPO in 2025.

Plaid aims to “revive growth” with credit underwriting, pay by banks, and “fraud.”

Underwriting has room to run, and pay by the bank will be competitive, but I think they should tokenize identity instead of trying to be another “KYC” player.

The single best growth opportunity in Fintech is emerging markets. W

e’ve seen LATAM and APAC. The next big market is MENA; the first two letters are “Middle East.” This week’s Rant is why you should pay more attention if you want growth.

PS. Something new this week. Rex Salisbury and I wanted to try something video native. You can see our first try below. Would love your thoughts 😊

🎥 Is KYC Screwed 👀

Here's this week's Brainfood in summary

📣 Rant: The next big Fintech Ecosystem will be the Middle East

💸 4 Fintech Companies:

Lab 1 - Gen AI for Data breaches in Cyber, Fraud & AML

Merge Money - The Cross Border API.

Sedric - A compliance copilot.

Datapher - AI Markets analyst Agent

👀 Things to Know:

📚 Good Read: Scaling AI

If your email client clips some of this newsletter click below to see the rest

Weekly Rant 📣

The next big Fintech Ecosystem will be the Middle East

In the past week both Revolut and Nubank announced expansion to MENA. Revolut secured investment from the UAE's sovereign wealth fund Mubadala and claimed to have 100,000 users on its waitlist.

My thesis is the next growth market in financial services is the Middle East. It already has regional powerhouses that have started to acquire European businesses and is becoming a gateway for global capital between east/west and G20 to global south trade.

These days, if you want to see the future of Fintech, you have to look outside the US and Europe. The largest digital banks are in APAC (Webank), and the most used RTP rails are in India and Brazil (UPI and Pix).

As many US investors have experienced, the rise of LATAM has been a game changer. And Asia’s Fintech scene doesn't generate nearly as many clicks as names familiar in the West and is consistently crushing.

But what about MENA?

I'm not alone in thinking it’s the next big growth market.

MENA’s largest economies are spending big to pivot from a 90% hydrocarbon-based economy to a services hub for the world.

It's different. It's top down. It's spending big, and its speed running from dumb money to smart money with brute-force cash injections.

But you cannot apply the lessons from India, China, LATAM, Europe, or the US to MENA.

Like every market, it has unique dynamics, energy, and opportunities.

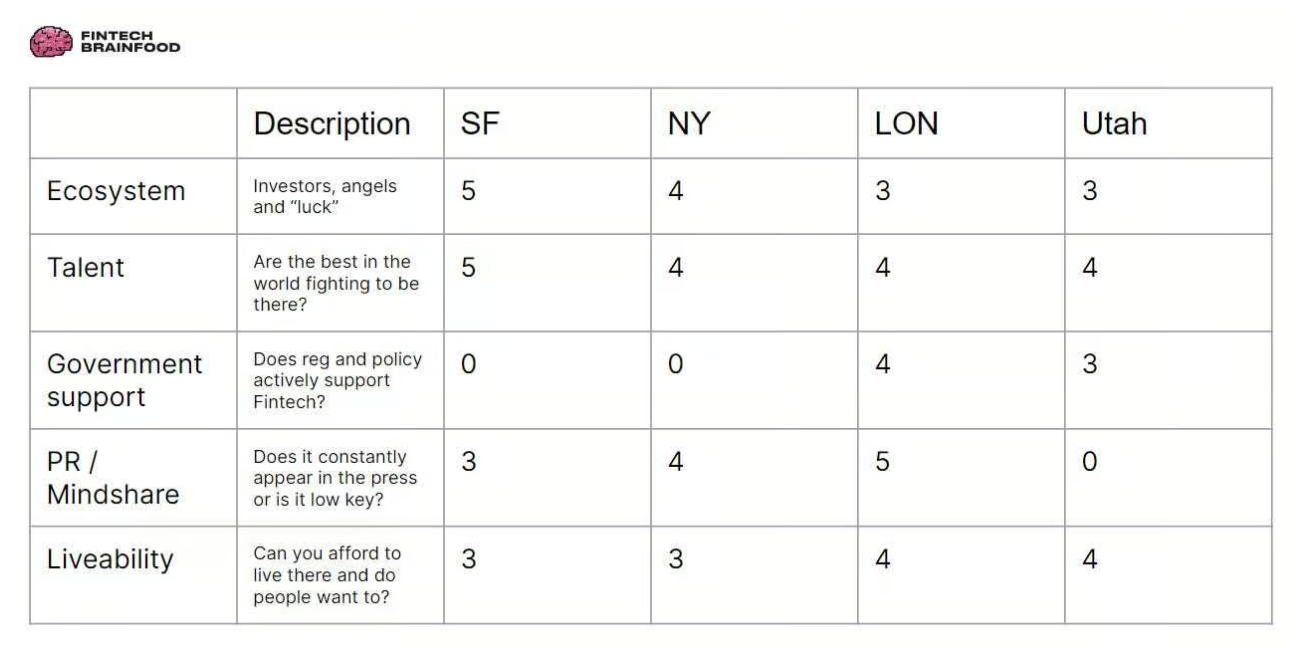

What does it take to become a Fintech Hub?

When I wrote about Utah earlier this year, I looked at 5 areas

Ecosystem: Will you bump into another founder, VC, or someone interesting in a way that feels like magic.

Talent: When you do, will that person be an A-player or a copy+paste business school type?

Government support: Uniquely in Fintech, the ability to get clear regulations is critical.

Great PR / Mindshare: Do you hear about it constantly, or is it understated?

Liveability: Does talent want to live and work there? Can you afford to start a family there?

As a purely subjective take this is what that looks like for NY, SF, London etc. (Btw, I'd edit these scores a little now, New York is currently the place for Fintech)

The hubs I didn’t include are the most helpful metaphors. Singapore and Hong Kong both act as off shore centers for the APAC region. As shipping hubs, they’ve both grown as global financial centers as Asia has risen from its currency crisis in the 90s to become the growth engine of the global economy.

They are similar but different.

Singapore with its proximity to markets with 100s of millions of users like Indonesia, and Hong Kong with its proximity to China. They’ve grown into technology and financial centers, and have been competitive on financial services regulation and Fintech for decades. While 10 years ago the UK was unquestionably the global leader in financial services policy, it’s now a 3 way tie between Singapore, Hong Kong and Abu Dhabi.

Both Singapore and Hong Kong host massive Fintech events, are global leaders in regulatory policy and act as hubs for global trade in and out of less developed local markets.

The Middle East as two leading financial centers

The UAE and KSA both see financial services as key to their future. They’re positioned as global shipping, financial, and technology hubs for the MENA region. The Middle East and North Africa have an estimated population of 493m across 21 countries.

While that’s not quite APAC’s 4.3bn people, if you exclude China and India some metaphors carry. There are markets like Egypt, Iran and Yemen that have users excluded from financial services, poorly served by incumbents and in need of solutions that suit their language and local needs.

The Middle East also more in the middle than London. If APAC is now the global growth engine, and the next growth engine is Africa, the ideal hub would be positioned where east meets west, and north meets south. There’s a rationale here to building a global tech hub that serves not just MENA, but global trade.

The United Arab Emirates (UAE) and the Kingdom of Saudi Arabia (KSA) are the most vocal and visible globally.

The UAE has been a first mover with Dubai becoming a global tourist destination. The Abu Dhabi Global Market (ADGM) has been a leader in new regulatory licenses. Meanwhile, it probably hasn't escaped your attention that Saudi Arabia is investing heavily in sports, infrastructure, and Fintech.

These are two wildly different markets in many ways. There’s a friendly competitiveness between the two centers each with relative strengths.

Two countries in MENA might break my scorecard. I thought I knew government support, but wow.

Here’s my rough take so far.

The UAE has significantly more existing momentum

Overview: The UAE has 9.4m residents, with 85% of those being expats or migrants.

As a center for Tourism, UAEs, Dubai has become a destination for creators and internet businesses for its low taxes and high-quality Western lifestyle. Abu Dhabi is positioned as a Singapore/Hong Kong style offshore financial center for the region, where global businesses like Binance are headquartered.

Abu Dhabi resembles Singapore in APAC as being no pushover with regulation but an innovator. It tends to regulate early, and thoughtfully and has consistently led the world in digital assets policy

The UAE’s sovereign wealth funds, such as AIDA, EIA, and Mubadala, have been active participants in their home country's development, foreign investment in VCs, and direct investment in growth startups (including Fintech in Mubadala’s case).

This model of using State funding to support the local economy as industrial policy is now a global default. In China, the USA and even Europe. The UAE was a leader in this approach.

Example companies founded there:

Tabby a BNPL provider founded in 2019, last raised in 2023 at a $1.5bn valuation. It was founded in Duabi (but has now moved to Riyadh) and became the first Fintech unicorn in the gulf region. With 10m users they’re not far behind Affirm and they’re profitable. They operate in a market where BNPL is seen as a more ethical way to manage cashflow, and where credit card penetration is low (averaging 10% regionally).

Tabby has also made tokenized payments at e-commerce and the wallet like experience a default for a region that had been slow to adopt e-commerce but is now shifting rapidly since the pandemic.

Qlub founded in 2021, raised $25m in 2023. Its QR code based restaurant payment service is now growing into a Toast-like vertical specialist payments company. The payment can still be with Visa, Mastercard, wallets or Mada. It’s an interesting hybrid of the QR-code obsessed APAC region, with the vertical integration we see with software-led payments companies in the West.

Alaanpay founded in 2023 is building Ramp for the GCC. Their home page literally says “Saving companies time and Money.” They offer spend management, accounting integration and manages VAT and tax reclaims. The quiet-part-out-loud of the GCC is being an expat and founding a business isn’t always easy. Alaan aims to help the freelancers and growth companies of tomorrow. Interestingly, Alaan too has now moved to Riyadh.

I could highlight literally 100s of companies here. Every other week I hear about some YC-backed company from the region having just raised.

Key things to know

Relationships matter. This is an incredibly outward facing, westerner friendly market. But it’s also one where scar tissue has been built up. If you assume you can show up and succeed you’re doing it wrong. The UAE is now competitive with any Fintech market for investor sophistication.

ADGM and DFSA are amazing if you’re a global enterprise. Both Dubai and Abu Dhabi operate regulators in a “financial free zone” This is separate to the main, on shore regulators. The central bank, securities and commodities regulator and FSRA regulate much of the local banking activity. These free zones manage more than 40% of exports (and continue to grow), and position the UAE for global trade.

Success in the UAE can be a launchpad. With a population of 10m most of whom are migrants, there’s a great opportunity to build wedge products. As many have found, this works in markets like Singapore as a base for talent to expand into the region. That’s not a guarantee, with large markets like Egypt proving difficult to penetrate (e.g. for Tabby), but it’s a great starting point.

KSA is a bigger home market and offers incredible incentives

Overview: The KSA has roughly 37m residents, with 40% of those being expats or migrants.

In recent years KSA has become a center for sports, attracting stars like Christiano Ronaldo and major boxing events. As a country with mountains, snow, beaches and desert it is now positioning itself as a global tourist destination. It’s second national airline Riyadh Airlines will launch next year aiming to compete with Dubai’s Emirates and position as a travel hub.

Global businesses like Uber have acquired homegrown companies like Careem, the regional ride-hailing and delivery giant. Some of the largest homegrown companies are Fintech companies that operate regionally (like BNPL provider Tabby).

As a financial services hub, the Saudi Central Bank (SAMA) is extremely risk averse and at the same time, incredibly innovative.

Example companies:

STC Pay was founded in 2018 and has been private since its inception. Today, it claims to have 10 million users and offers wallets, local and international transfers, and bill pay. It also enables small and micro merchants to accept payments, manage their finances, and take stock. It looks a little like a local version of Block, with a consumer—and merchant-focused business offering. It’s at scale, successful, and starting to unlock regional ambitions.

In a market that is 40% migrants or expats, poorly serviced by the large banks, STC Pay carved a niche as being actually capable for this audience.

Tarabut is the Plaid for the MENA region, raising a $32m Series A in 2023 after founding in 2017. Investors include Visa and Tiger Global. They do account verification and validation, payments, payouts, and all of the data categorization you’d expect. There’s a ton of local nuance, however. When we say “Open Banking” in the West we think screen scraping then tokenization.

The significantly more data privacy and data residency-centric KSA thinks about incredibly secure data access and management. Despite offering a working payments product, the primary use case so far has been as a dashboard for potential future lending (think Petal and scoring). Expect this to change as the KSA is due to pass open banking regs soon. The twist here is that Tarabut has built a product that could start to work regionally.

Barq is the fastest-growing digital wallet outside of China. In less than 30 days, it hit $1 m users. The timing is perfect: The major cloud service providers have just arrived, the central bank is supportive, and the CEO is the former CEO of STC Pay. Still, even with all of that at their backs, Barq is experiencing incredible growth.

Their ambition is to become the first true MENA regional wallet. Their “spin the wheel” approach to cashback is surprisingly popular, with users given the chance to win up to 100% of cashback on purchases. It comes with a Visa card, P2P transfers, and cross-border baked-in. If STC Pay looked a little tired, Barq looks as good as anything in the world. KSA has been yearning for this level of quality in execution. Perhaps they’ll break the ice for many others to follow.

In theory you could claim Tabby and Alaan are now KSA companies since they moved their HQ there. A little like how Tesla moved it’s HQ to texas. You follow the incentive.

Key lessons from locals.

Build with the infrastructure not against it. KSA has a national digital identity service making KYC much simpler. There are now finally cloud service providers with in country data centers. The timing is good to work with what’s there.

The incumbents aren’t competitive. The large banks have innovation arms that are starting to make some interesting moves, but as yet they lack traction compared to STC Pay or Tabby.

It’s harder to make money with cards-first. Saudi’s payments network Mada (under Visa and Mastercard) is capped at 0.8% on debit.

BNPL works well because it’s seen as ethical and has a dedicated licence from SAMA to streamline things.

Don’t say BaaS or embedded finance; do say wallet as a service. SAMA is incredibly risk-averse by global standards. If a regulated bank or wallet offers that wallet “as a service,” however, that’s more acceptable.

Open Banking is taking longer than everyone wants. Just like 1033, or Open Banking in Europe, deadlines get missed. But Tarabut is successful, connected to banks across Bahrain, but KSA requires regulation. Everyone is waiting, but Fintech companies are running out of cash. Watch this space.

Weighing them up

With all these things it’s tempting to say there’s one winner and one loser. The reality is they’re different.

UAE’s market-led approach to regulation appeals to international innovators. ADGM and DIFC are creating the leading regulatory frameworks globally.

SAMA is policy led. Giving big liscences one it’s comfortable with risk. While SAMA is much more cautious in KSA, it also represents a very large home market and the potential to build winners that could spread regionally.

The UAE has become much more liveable for expats and has a stronger talent density. While the KSA is offering incredible incentives, and investing in its long term liveability for talent.

Perhaps the UAE’s policy-forward approach will appeal global enterprises, while KSA’s larger home market and incentives will create regional stars.

The reality is they’re both poised to do well as the MENA region begins to rise.

These things are never static and are subject to change (hence the little arrows in this picture).

We haven’t yet seen big Fintech exits, partly because there’s a nascent local capital market, and partly because we’re still early. But at the rate Tabby is growing, who knows how long that will be true for.

Lessons for the West

Defaulting to cynicism is a mistake. Dubai's influencers and KSA's “Line”, which has gone from 170km to 2km, are all as meme-worthy as they are cringe-worthy.

Defaulting to being judgemental is also a mistake. In a polarized world, we forget that Blackrock is now leading major regional public infrastructure investments. We get lost in memes, YouTube videos, and clickbait.

If that's all you see, you're missing the big picture.

I don't think anyone from the UAE or KSA is pretending their projects to transform their economies are finished or perfect.

Far from it.

A. Lean into the ambition. Imagine living in a country with the ambition and capacity to build incredible things, not just in physical infrastructure but also in regulation. In Europe, we'd be bogged down in regulation before an entrepreneur had their breakfast croissant. Everything in the US would cost 100x more, requiring 50 State licenses.

These are markets where you'll get $2m to locate your headquarters in KSA and base your team there. Where Fintech is a strategic sector, and the central government and central bank has a goal to increase the number of jobs, companies and contribution to GDP.

B. Lean into regulatory support. The Abu Dhabi Global Market (ADGM), Dubai International Financial Center (DIFC), and Saudi Central Bank (SAMA) are regulators with a mandate to support Fintech company growth. Their governments fully support the development of Fintech ecosystems.

These are markets where Fintech is not a dirty word (like Washington). That doesn't mean the regulators will give you an easy time. By global standards, SAMA is strict on loan loss ratios and how interchange can work. Remember too, there's Sharia to consider, which makes lending compliance and economics more nuanced.

C. Leave your assumptions at the door. Don’t expect SF like talent density or New York style networking and deal making. If there’s one thing every college educated, global citizen from the Middle East gets frustrated with it’s the “fly in and fly out” westerners who show up, look to do business and leave.

By the same token, the UAE has an ecosystem of serial entrepraneurs who have $bn exits and are building their next thing. “Founder mode” is alive and well in the KSA too. There is greatness here, you just have to invest your time to find it.

A good friend of mine Leda Glyptis is a veteran of the wider region, having been Chief Digital Officer for QNB in Qatar in the mid 2010s. Her experience of KSA was “this is very different.”

Don’t expect home. Don’t expect perfection. Show up with humility.

D. Relationships matter. This is a culture with a genuine warmth and love of their friends and colleagues. It’s also one where a handful of people in senior positions operate on trust and over longer time horizons. Partly as a defense against the fly-in, fly-out crowd, but also as way to ensure business transactions can be trusted.

When you hold a lot of money or policy power, everyone looks at you like the kid holding a jar of sugary snacks. You have a right to be a little cautious. There’s also the nature of local regulations. As a region that’s witnessed global Fintech develop, they’ve seen the good and the bad. There’s a desire not to see a Synapse-like situation or the fraud issues in real-time payments.

Does the global Fintech company looking to launch in MENA understand that? Or did they just get an investment from one of the larger funds and see an underserved population of 500 million people?

Is there really something going on or is it all bought attention? It's real -- Here's why.

I put this Rant together for several reasons

I was invited to speak at Fintech24, an event in KSA roughly the size of M2020 in Vegas.

I noticed familiar names like Matt Harris from Bain Capital, Sheel Monhot from BTV, and Professor Chris Brummer speaking.

They had their Central Bank Governor speaking. This would be like Jerome Powell speaking at Money 2020.

My network has been telling me that "there's really something going on in Saudi Arabia,"

I wanted to see it with my own eyes. Is it all people showing up for the cash, or is something real going on?

The short answer is there's something very real happening.

Much of it is funded with state cash, and success relies on knowing the right people.

But there's also a genuine set of entrepreneurs and companies that would be competitive in any market on the global stage.

In 2015 I remember meeting an employee of the Monetary Authority of Singapore (MAS) who described their job as business development. Their goal was to attract global Fintech companies to setup in Singapore as part of their global expansion. In 2016 I visited KSA for the first time and remember thinking, yes, this is a very different market.

Nearly a decade later I find myself with a blizzard of invites to conferences and Fintech events in the MENA region, fresh from Fintech 24 thinking, ok things are changing.

That doesn’t mean they’re perfect or the finished article. Far from it.

But if you want to look for growth right now, look east. Turkey’s economy is in the toilet but its Fintech companies are on fire.

The biggest Fintech growth story in history could be in front of us.

And that.

That is worth taking a proper look at.

ST.

4 Fintech Companies 💸

1. Lab 1 - Gen AI for Data breaches in Cyber, Fraud & AML

Lab 1 continuously monitors exposed data and can provide impact summaries to organizations. The platform lets users search by their organization or executive names to find impacted artifacts (like emails or documents). Then, the service provides an AI-generated summary of the exposed item without revealing the PII or sensitive data itself.

🧠 The alternative to Lab 1 is to hire a team of analysts. (This is how Recorded Future, acquired by Mastercard for $2.6bnn, works). Analyst teams can take weeks to respond to new breaches and often miss key bits when sifting through terabytes of data. AI fixes this and summarizes the impact instantly.

2. Merge Money - The Cross Border API.

Merge provides an API for multi-currency accounts, global real-time payments, and funds storage at either the Bank of England (Central Bank) or JP Morgan. They serve marketplaces, Fintech companies, wealth managers, and payroll companies. The team is ex AliPay, Coinbase and PayPal.

🧠 Fintech still isn't default global. While great companies like Nium, Routefusion, and Airwallex exist, there's still an opportunity in the sort of "BaaS for cross-border." Virtual IBANs, segregation of accounts, automated FX. Could be one to watch.

3. Sedric - A compliance copilot

Sedric helps convert policy documents into processes, automate some execution, and manage compliance reporting. The service reviews 100% of customer interactions in 40 different languages to ensure compliance policies are upheld.

🧠 The policy-to-production pathway is neat. An LLM's ability to read a policy document is helpful; it can then ensure it is applied in unstructured customer comms, marketing, etc. These interactions are fewer numbers or data-driven and more judgment-based. This makes you wonder if the LLM understood the policy. There's some interpretation happening. I can see why this appeals to overworked banks worried about the next compliance fine, but I'd want to really kick the tires on something like this.

4. Datapher - AI Markets analyst Agent

Datapher is an investment analyst agent that automates research and analysis tasks. Users can ask natural language questions about historical market data, get 5-minute summaries on the market relevant to their portfolio, and update models with live data.

🧠 Datapher claims to be significantly more accurate than GPT4o in Finance bench. Specialized models still have an edge regarding data tasks (although o1 may change that). The human experience of being an analyst and responding to professionals' questions isn't readily available in training data.

Things to know 👀

The DoJ says that Visa, with a 60% market share, uses bulk discounts and incentives to ensure merchants route debit payments via its network in the United States. The complaint also says Visa offers incentives for potential competitors to collaborate.

🧠 What has Visa actually done wrong here? There's no question Visa has a dominant market share in the US. But $0.03 on a $0.25 fee is not "abusing" the market unfairly.

🧠 The complaint concerns Visa's commercial incentives for partners. You get bulk discounts if you do more with Visa. That's not anti-competitive, it's capitalism. You get an upside if you partner with Visa. Again, capitalism.

🧠 Visa and Mastercard are increasingly vulnerable to new rails. Pay by Bank, RTP, and international competitors like Pix, Alipay, and UPI have competing numbers of consumer users. The opening of NFC on the iPhone means every wallet could have every rail available to everyone.

🧠 Hurting Visa hurts the US payment's global competitiveness. Card networks are not the dominant form of payment in APAC, and Visa is not dominant in Europe

🧠 This move by the DoJ is myopic and US-centric. India is intentionally bringing UPI to the world, and the BRICS are trying to build a SWIFT alternative.

In 2021, Plaid raised $425m at $13.4bn, making the CEO a paper billionaire. Since then, Fintech valuations have normalized, with secondary markets pricing it at $3.8bn, and Plaid’s growth has dropped to a more moderate 20% YoY. It’s not yet profitable (will lose $50m in 2024) but is trending that way. It is pushing Pay by Bank, Credit underwriting, and Fraud detection to drive growth.

🧠 Any company doing 20% YoY revenue from a $308m base is doing something right. Let’s take a second to recognize that this is the company everyone in Fintech owes a debt to. Modern onboarding in the US, modern fraud detection, cashflow underwriting and pay by bank are all mainstream because Plaid executed well.

🧠 Plaid created a verb and a company category but not a business model. Plaid data is a must for any Fintech company and anyone optimizing conversion at onboarding.

🧠 They saw their Fintechs as customers and banks as data pipes. This created bad experiences, and banks fought back, “breaking” Plaid connectivity and allowing older competitors like Finicity, MX, and Akoya to gain share. This has changed; relationships are better, and banks now have APIs, but then regulation happened.

🧠 1033 arguably commoditizes Plaid’s data provision business. If every bank must make data available, having a brand and good bank coverage is no longer a winner-take-all market. Plaid has to move upstream to find value.

🧠 Plaid still has breadth and network. It has more connected accounts and more data than any other aggregator. Having a network is a great head start if you make AI models for underwriting, fraud, or risk.

🧠 The question is, can they capture identity from the network? Or will identity live in wallets like Apple Pay or services like CLEAR, with Plaid as a data provider?

🧠 The future of underwriting is more data - they might have something here. Cashflow underwriting is incredible, and we’ve barely scratched the surface of its potential. There are companies built on Plaid that clean data for credit, but they are not CRAs. If I had 100s of millions of transaction bits of data, I’d love to build a synthetic version, and start testing cutting edge models against that. This could be huge.

🧠 Payment companies like Fiserv might better serve Pay by Bank than aggregators. Walmart uses Fiserv, which connects to all the account aggregation services to enable Pay by Bank. Plaid has distribution and mindshare, but that doesn’t guarantee volume. Still, Pay by Bank will have meaningful upside if Plaid can capture market share. Partnerships for Pay by Bank will be a key battleground for the next 3 to 5 years.

🧠 Plaid might own identity but not fraud. Fraud is a huge hot-button issue, and it’s how you sell identity and KYC tools, but it’s a much bigger problem than offering onboarding. The article mentions competing with Socure, which does KYC but has 20 other products. Plaid has unique data but also makes most of its money selling data to fraud detection and onboarding solutions. Therefore, their fraud solutions compete with a segment of your customers; they will have a capped upside. That’s missing the point, though.

🧠 The big play for Plaid is tokenizing identity in its network. However, if they tokenized identity like they tokenized payments for pay by bank. That would be interesting. They could sell that to any Fraud vendor, financial institution, etc.

Plaid is an identity company.

PS. Is Jeff Kauflin the “Hey, we need an IPO piece” guy now? First Chime, now Plaid?

Good Reads 📚

1. Scaling AI

AI scales with more than compute. While models will get bigger, they're getting more efficient and effective too. Ethan presents three generations of models

Gen 1: ChatGPT from 2022 to early 2024

Gen 2: Frontier ChatGPT 4o, Claude Sonnet 3.5, Llama 3, Grok 2

Gen 3: GPT5 et al

Gen 4: About 2 years out

Ethan speculates that getting to a Gen 4 model will cost about $10bn in training, as the Gen 2's are at least $1bn in raw data center cost. The reality is there is enough cash for this.

🧠 So much of what we assume to be true about GenAI is changing. The sands are constantly shifting. Every company building in this space constantly changes, tweaking and optimizing its stack as new things emerge.

Tweets of the week 🕊

That's all, folks. 👋

Remember, if you're enjoying this content, please do tell all your fintech friends to check it out and hit the subscribe button :)

(1) All content and views expressed here are the authors' personal opinions and do not reflect the views of any of their employers or employees.

(2) All companies or assets mentioned by the author in which the author has a personal and/or financial interest are denoted with a *. None of the above constitutes investment advice, and you should seek independent advice before making any investment decisions.

(3) Any companies mentioned are top of mind and used for illustrative purposes only.

(4) A team of researchers has not rigorously fact-checked this. Please don't take it as gospel—strong opinions weakly held

(5) Citations may be missing, and I've done my best to cite, but I will always aim to update and correct the live version where possible. If I cited you and got the referencing wrong, please reach out