Welcome to Fintech Brainfood, the weekly deep dive into Fintech news, events, and analysis. You can subscribe by hitting the button below, and you can get in touch by hitting reply to the email (or subscribing then replying)

Hey Fintech Nerds 👋

Circle had the blockbuster IPO of IPOs. From $31 to over $100 in its first day. We’re in a stablecoin supercycle, and every corporate treasurer and PSP is talking about it. It’s all anyone could talk about at Money 2020 in Amsterdam. (See Things to Know 👀)

To deliver on their promise, stables need the GENIUS Act to pass. Then institutions will mobilize. Consider that the Bitcoin ETF happened in Jan of 2024.

A story that hasn’t been covered much is Visa launching A2A, “with guarantees.” They’re bringing scheme protections like fraud, chargebacks, and rules to pay by bank in Europe. Huge moment.

This week, my Rant is based on the BCG x QED report. Fintech is still 3% done despite growing revenues by 21% and EBITA by 25% YoY.. With big IPOs coming, Agentic-first companies emerging, and stablecoins reshaping the infrastructure, the next phase is going to be much bigger.

The lesson from the crypto industry is that policy engagement pays off.

If you care about preserving open banking, regulation for earned wage access to the future of who gets to have a charter, you absolutely have to get to the Fintech Association (FTA’s) CEO summit on June 25th in D.C.

Here's this week's Brainfood in summary

📣 Rant: Fintech is still 3% done.

💸 4 Fintech Companies:

Atticus - The Neobank for Defense(?)

Velocity - The FX Platform for Stablecoins

Ontik - Payment ops for B2B trade wholesalers

Truemarkets - Interactive Brokers for Crypto

👀 Things to Know:

Using Gmail? - You’re missing 75% of Brainfood. Click here or below to Read Online

Weekly Rant 📣

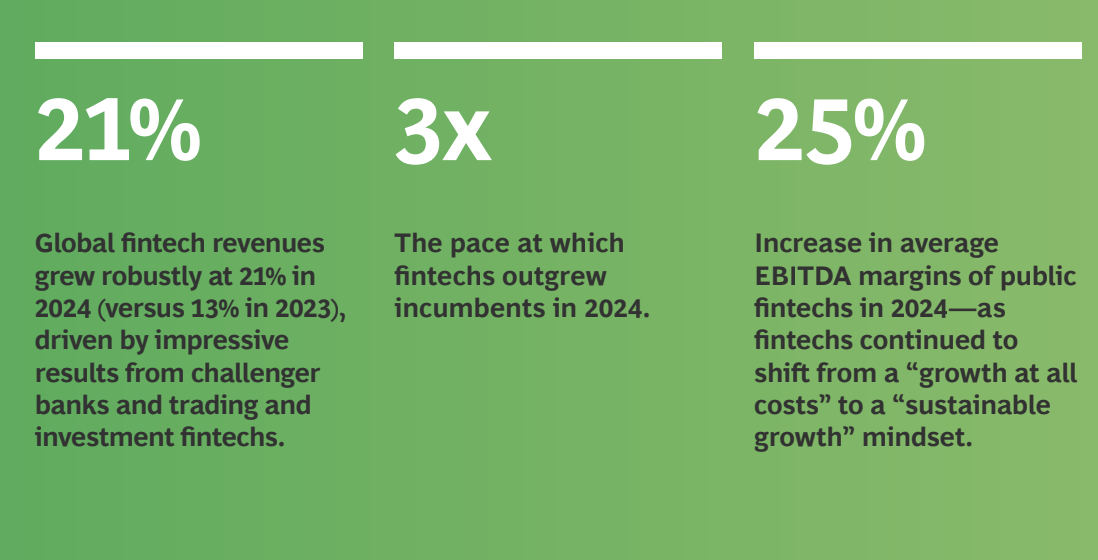

Fintech is still 3% done.

Good things come in threes.

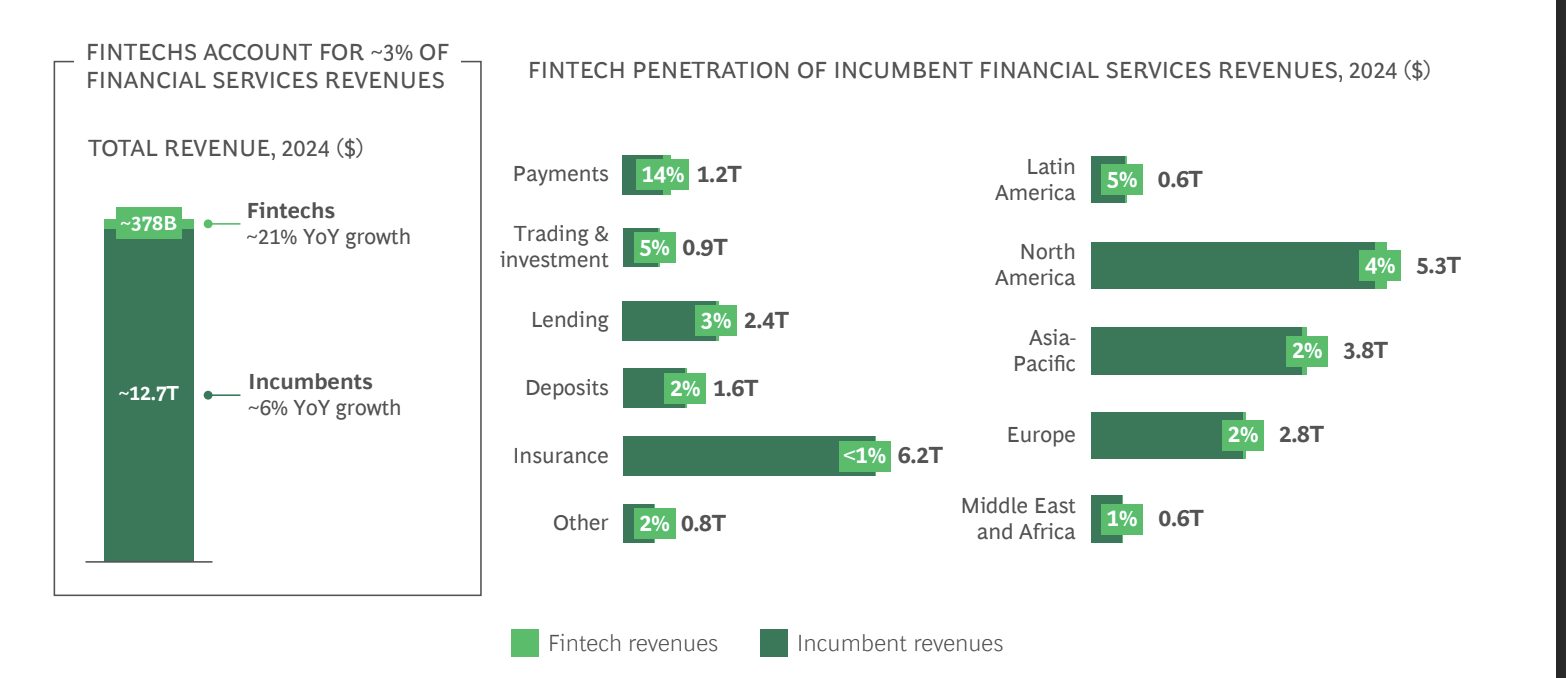

In 2024, Fintech companies grew revenue 3x faster than incumbents at 21% YoY, they grew EBITDA by 25%, but still represent only 3% of the financial services market cap.

That 3% figure tells you everything about where we are in this story. We're not at the end of the fintech revolution, we're barely past the opening credits.

The data from 2024 shows an industry hitting its stride just as the next wave of disruption begins. While Chime, Circle, and Klarna prepare for IPOs that could shift that market cap percentage slightly, a new generation of AI-native companies is coming up from below, changing the rules entirely.

Scaled Fintech companies go public, cross-sell and go global

A new generation of AI-native companies is coming bottom up, changing everything

Fintech is a State of Mind

The report suggests fintech wins where banks are uncompetitive, unwilling, or unable to compete. That's true, but incomplete. It misses the how.

Every incumbent has APIs, mobile apps, and cloud migration strategies. But having technology is like owning running shoes, it doesn't mean you know how to run. For most incumbents, those shoes are gathering dust at the bottom of a cupboard.

I spoke to a C-suite banker this morning who lamented having "product people" who don't think with a product mindset. They manage P&Ls and internal processes to deliver features. That's project management, not product thinking.

Fintech companies, in general, have a lower regulatory burden and lower cost to serve. This explanation misses an important element. How is their tech, op model, and regulatory approach different?

Contrast the two mindsets.

The CEO regularly reads complaints to drive the roadmap. In my interviews with the CEOs of Ramp, Brex, and Mercury, all three founder-CEOs did this. They see any customer pain as critical. (I see this daily at Sardine* too)

Customer complaints are a separate department. Service management picks up those complaints and runs them through a “voice of customer” program so we can make sure we’re reporting to regulators what happens.

For Fintech companies, they’re mobile-only, cloud-only, and API-first.

It’s hard for me to express how much this impacts everything.

If your product people don't know which screens create drop-off, or how tiny changes in app responsiveness affect customer stickiness, and drive down CAC. You're not building products, you're building features. If that feature is 3 clicks down and barely marketed, it may as well not exist.

Fintech wins because they have a product mindset.

Come meet me, and your favorite Fintech leaders, operators, and founders in Miami at Fintech Nerdcon 👇

Want to be around the best in the industry? Grab a ticket ASAP.

Fintech Companies are growing 3x Faster

Growing 3x faster than incumbents while expanding EBITDA shouldn't surprise anyone. But sustaining that while moving upstream into traditional banking products?

That's new.

Look at all that white space to attack

Digital-first B2B brands started with simple debit cards and are now building full-stack banking. Revolut has 50%+ market share in some European markets and is expanding into mortgages. In a decade, that market share graphic will look very different.

Meanwhile, Payments is 14% done.

Stripe, Adyen, Checkout, and their ilk have taken a meaningful bite out of the payments acquiring market. Incumbents in this sector are mostly sitting ducks, using M&A as a primary way to fight back (although stablecoins might help).

But core profit centers like lending, deposits, and insurance are nowhere. Why?

These sectors have had less of a secular trend, like mobile commerce or e-commerce, to drive them. These sectors lack the secular tailwinds that drove payments (e-commerce boom) and lacked simple wedge products (Square's card reader for micro-SMBs).

Deposits and AUM compound. Incumbent customers skew older and higher income. Those later-in-life customers have higher deposit bases. Banks that have been around longer have had more decades to grow their deposit base. Why? Some of this is product-fit; they have more appealing pricing and offerings. A lot of it is the inertia of this segment.

Digital-only B2B brands are only just starting their product expansion. What began as very simple debit-card products is slowly becoming as feature-rich as the incumbents.

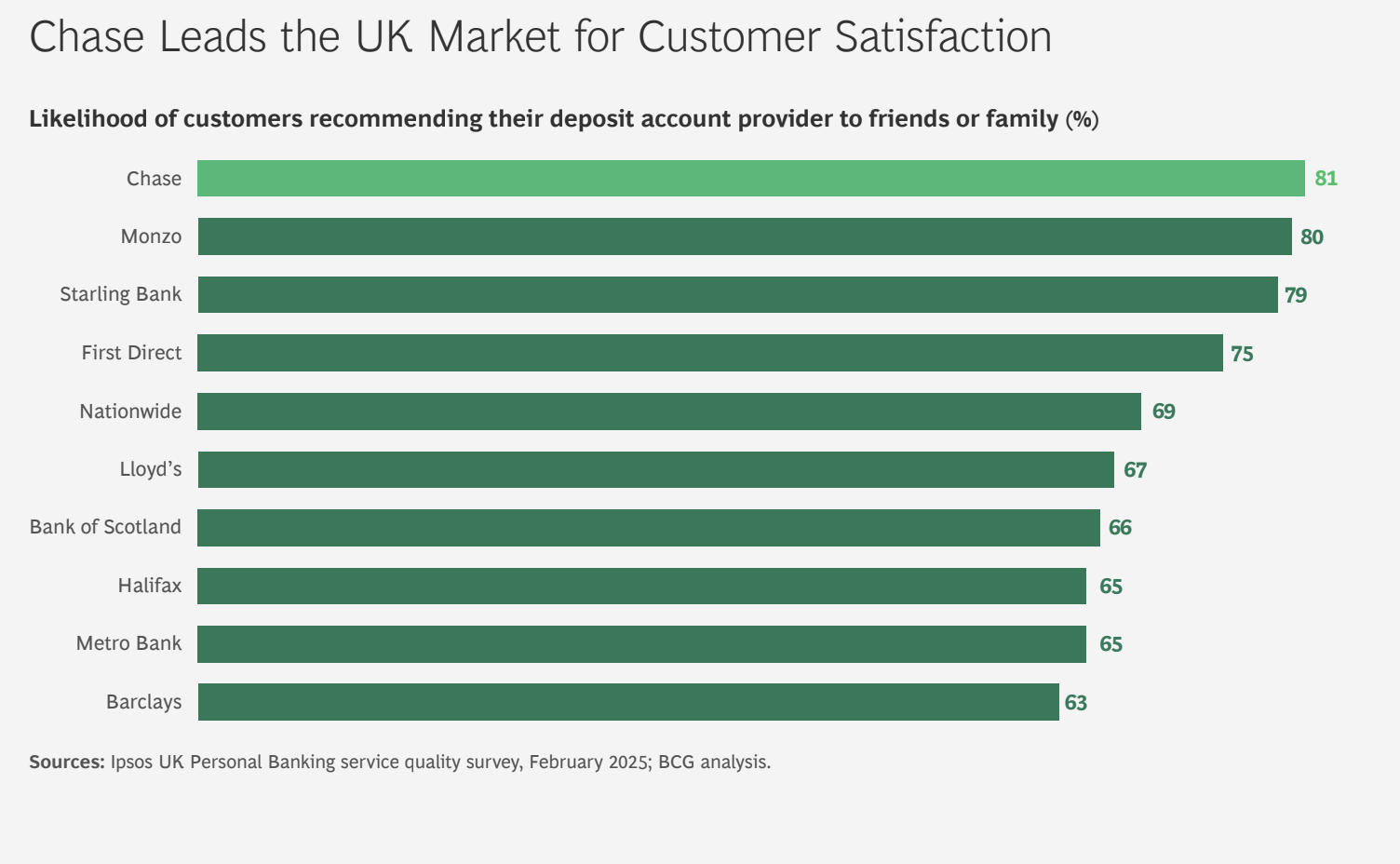

The incumbents aren't cooked. AMEX and Chase are winning with affluent Gen Z, and Chase UK actually beats its challengers on customer satisfaction. But the minimum viable product has permanently shifted.

Having a terrible app is no longer an option.

Incumbents can do digital and win

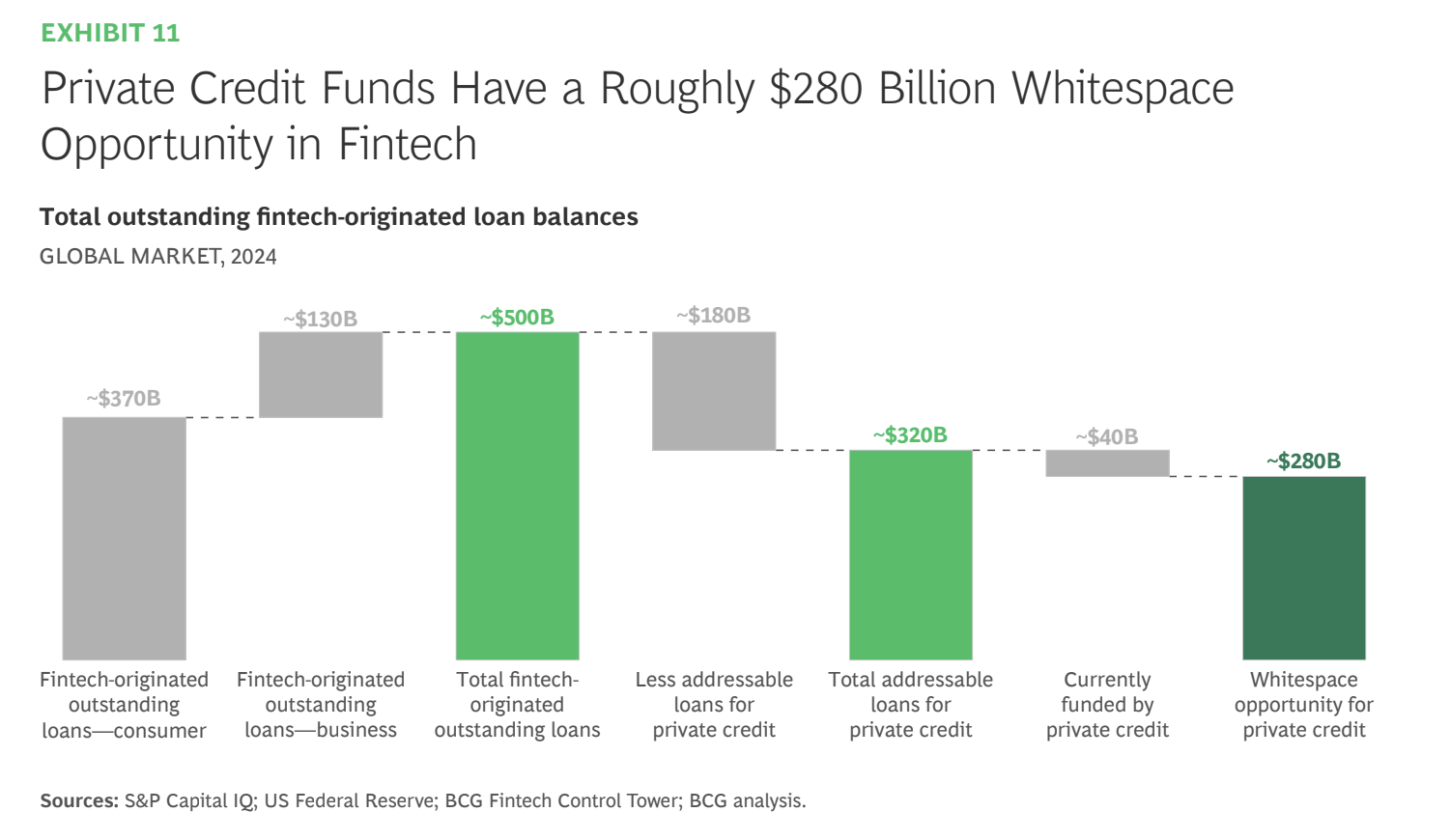

Private Credit Momentum in Fintech is at an Inflection Point

Banks built their moat on cheap deposit funding.

Private credit is dismantling that advantage.

SoFi and Klarna recently announced major private credit partnerships. Funds like Blue Owl see the opportunity and are deploying capital to fintech at scale. We're in the early innings of this shift.

Side note: Banks worry about stablecoins creating narrow banking while private credit, the actual existential threat, operates largely outside banking capital adequacy regulations. When banks complain about an unlevel playing field, they're not wrong.

Cheap funding isn't the only advantage being dismantled.

The innovation cycle itself is accelerating.

Agentic AI is in production in Fintech companies

Fintech companies can adopt innovation faster than incumbents.

The BCG report speculates about future AI use cases, but that misses what's happening today. AI agents aren't coming to fintech, they're already in production, making decisions.

Every ops team will have Agentic AI hires helping them. Two years ago, I wrote “from outsourcing to AI sourcing.”

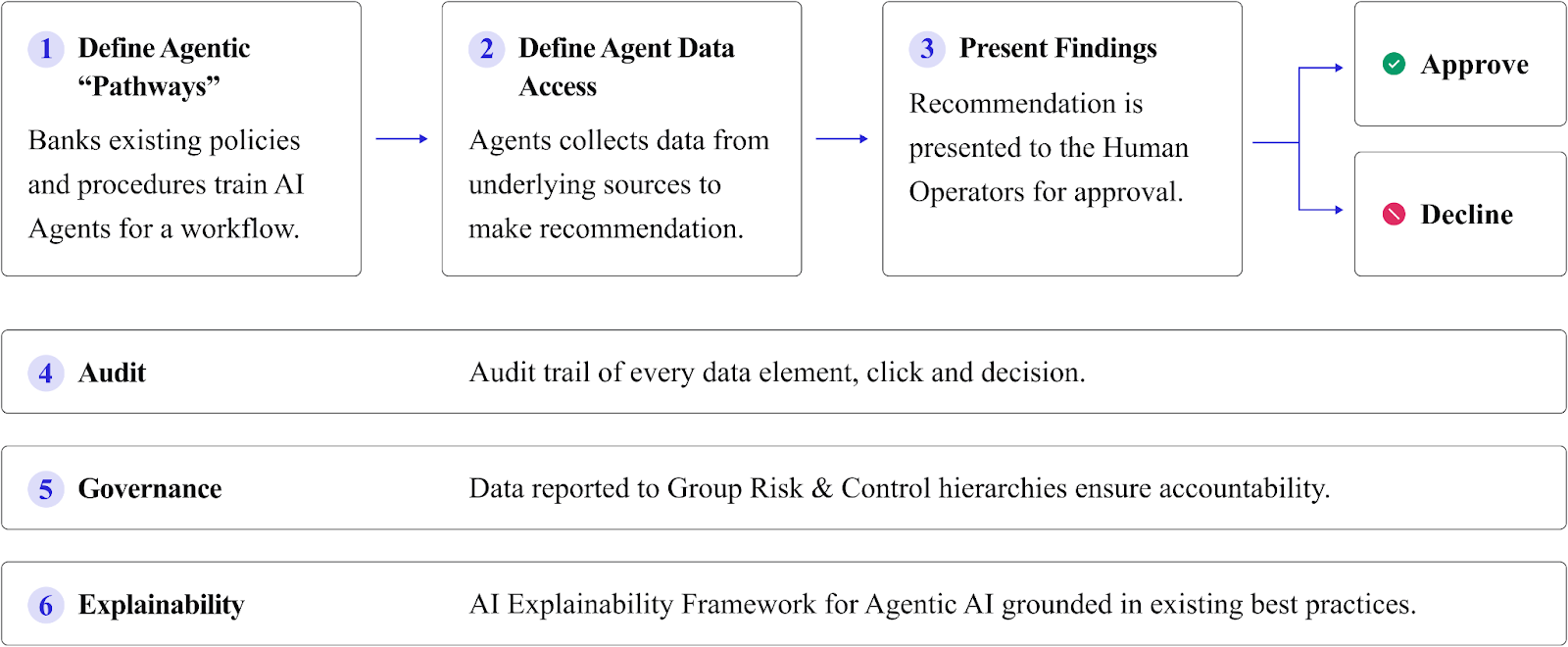

To get an LLM to follow an organization's policies or processes, it first needs to understand those processes

It turns out that was absolutely the key.

Every IT Department is becoming an HR department for AI Agents. Think of it like onboarding a human agent

You need to define their job description

You need to give them procedures and policies (employee handbooks etc)

When they do the job they might need sign off internally or reviews

This is live, in production, today. As we discussed in the Sardine* Agentic Oversight Framework whitepaper:

We're already seeing remarkable results:

Queue resolution rates for AI agents vary by use case. For KYC workflows, resolution rates exceeded 98% on average. For more complex tasks, such as sanctions screening or negative news reviews, resolution rates were closer to 55%. Alerts that were not resolved by AI were then escalated to human reviewers.

The most counterintuitive finding in that paper? AI agents are more consistent than humans at resolution.

Standard Operating Procedures have become the secret weapon. LLMs consume them like I consume Pepsi Zero, and suddenly, complex compliance workflows that took days now take minutes.

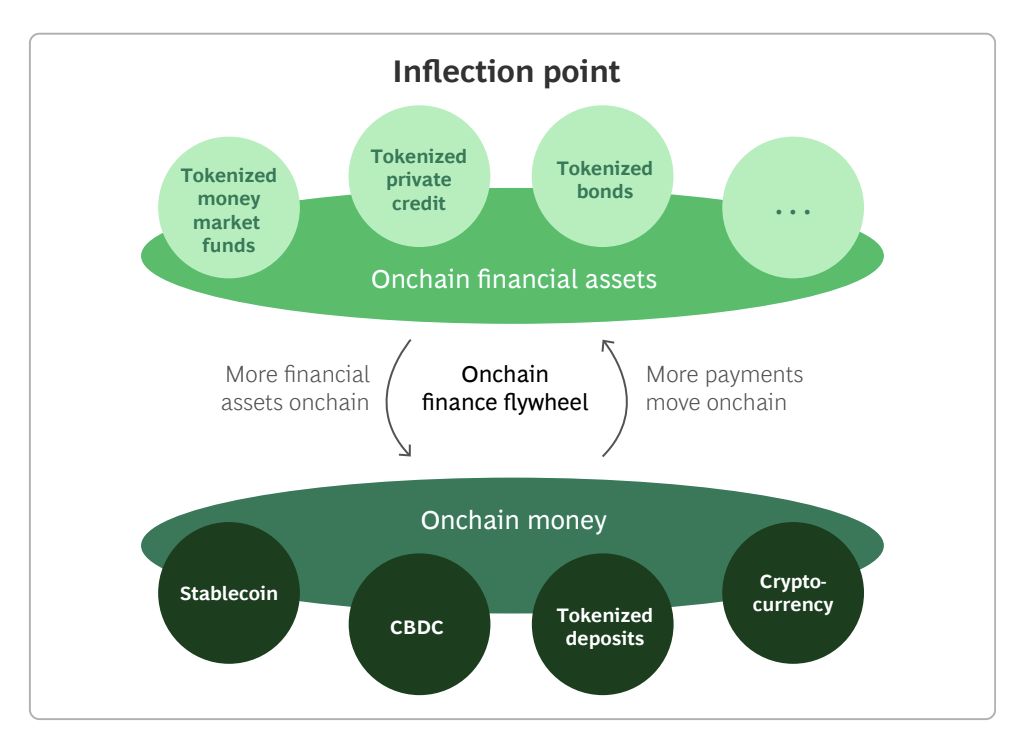

The on-chain flywheel has started

Tokenized assets hit $600bn in 2024. That's still small, but the trajectory is unmistakable. Tokenized assets will be much bigger than stablecoins.

What’s interesting to me is we’re now talking about ”onchain” finance which even 3 years ago would have been crazy. It also seems to be a term the tech and finance world are both cool with. No bifurcation nessasary.

The most interesting thing is who's driving growth. The buy-side (Franklin Templeton, BlackRock, WisdomTree) is leading with tokenized money market funds and is increasingly adopting everything else. They're expanding TAM by taking US onshore assets global, just like stablecoins did with the dollar.

Think about that for a second.

As the world goes to private credit, the same funds are lining up to take advantage of tokenization. As tokenized assets, stablecoins, and money market funds (MMFs) mature, they're displacing both sides of bank balance sheets.

Two forces are converging:

Bottom-up: L1 protocols, DeFi projects, and startups tokenizing every asset class

Top-down: Traditional market infrastructure (DTCC, Euroclear) building scalable tokenization

Now these worlds are converging.

These things happen slowly, then suddenly.

We’ve had a couple of false dawns with tokenized assets, and we’re not out of the woods yet, but I can’t see how the GENIUS act is anything other than a massive inflection point.

Adaptability is your Moat

There's an argument that AGI arrives by 2025, making predictions pointless. Maybe. But that uncertainty itself points to the one skill that matters over the next decade: adaptability.

Not just learning new tools—adapting fast enough to capture opportunity without losing what makes you special.

Personal level: Questioning experience and biases, especially for those of us who've been around long enough to think we know how things work.

Organizational level: Adopting new capabilities without breaking existing strengths. Moving fast while maintaining culture.

By summer, we might see GPT-5. It could change everything again.

If 3% of your workforce has access to ChatGPT and less than 3% of your infrastructure is cloud-native, you won't be competing in the next decade. But if you can adapt continuously while staying true to your core mission, you capture the upside.

Side note: There’s a lot of doomerism about entry-level jobs going away to AI. But young people are the most adaptable by default. What they need is a network and industry context. That’s my mission for the next decade.

The 97% Opportunity

The vast majority of finance is still paper, people, and process.

The Fintech roadmap drives directly into that opportunity.

Fintech companies cracked the code on product thinking, customer obsession, and rapid iteration. Now they (and bottom-up competitors) are adding AI agents, private credit partnerships, and on-chain infrastructure to that foundation.

The incumbents with deep customer relationships and regulatory expertise aren't dead. But they need to learn how to run in those shoes they bought.

The next decade belongs to whoever can adapt fastest while keeping their soul intact. The 97% of financial services still up for grabs will go to those who master that balance.

If you’re adaptable, as a leadership team and individual.

You win.

Stay curious. Keep learning. The game is just getting started.

ST.

What market signals are you seeing that suggest we're moving faster or slower than this trajectory? Hit reply. I read every response. (Yes really)

4 Fintech Companies 💸

1. Atticus - The Neobank for Defense(?)

Atticus is a company that appeared to be a consumer Neobank built on stablecoins after a seed round in early 2025 which was to value them at around $50m post. However Axios is now reporting that Palmer Lucky (of Anduril fame) is personally leading a new round at a whopping $2bn valuation.

🧠If you connect this to the “de-banking” narrative, then is this a “bank for the defense industry” of sorts? The Anduril involvement suggests this team would have access to the Trump administration and the ability to secure difficult contracts with government. I wonder if this is aimed to be a USAA competitor, or something that serves the broader supplier ecosystem. The door is certainly more open than it has been in a long time for Federal Charters, and there’s a lot of directions that could go. I could imagine an instant, 24/7, dollar-based bank would be very interesting for companies like SpaceX and Anduril, who operate internationally by the nature of what they do.

2. Velocity - The FX Platform for Stablecoins

Velocity is an enterprise-grade treasury management platform that helps connect ERPs (e.g. Kyriba). The goal is to give corporate treasurers the benefits of stablecoins (instant, 24/7, cash-like payments), with all of the scale and tooling they expect and need to be able to use. The founding team has senior leadership experience at FIS, and seasoned serial entrepreneurs.

🧠 Enterprise corporate treasury is the next unlock for stablecoins. B2B cross-border is the fastest-growing use case in stablecoins, but to get to scale it needs the tools enterprises would expect. It must be able to handle large payments and offer at least the same foreign exchange rates that these companies receive in an Interactive Broker account.

3. Ontik - Payment ops for B2B trade wholesalers

Ontik helps suppliers in trade, like building materials companies, manage their buyers either via cash accounts or with a line of trade credit. Users can send fully branded payment links via mobile phones, track views, automate follow-ups, and then manage payments via cards, open banking, or mobile wallets. This is then all reconciled against the company’s existing back office.

🧠Tradespeople live in mobile, email was sub optimal. What’s interesting about this is its a UK-centric app. You’d expect default mobile as a value proposition in some parts of the world. But getting supplies for a big job, and then being on the job, are less laptop and email-compatible.

4. Truemarkets - Interactive Brokers for Crypto

Truemarkets gives access to “institutional-grade markets” from a mobile app. Users can track trending assets and execute complex strategies simply. This sits in front of TrueX an exchange that offers pro features like separating execution from custody and a low-latency API for precision trading.

🧠The fall of FTX left a gap in the market for the high-performance crypto platform. FTX was both loved by traders and the mass market. Precisely because it was so high-performance.

Things to know 👀

Circle just raised $1.1BN in pre IPO sales, $31 per share, $6.9bn valuation. At the time of writing (6th June), it is at $94 in pre-market, valuing the company at $16.6bn

🧠 Circle is the stablecoin stock. Where else do public equities investors go to get exposure to the “stablecoin supercycle” that kicked in since Stripe acquired Bridge?

🧠 This is a huge moment for stablecoins. At Money 2020, it was all anyone could talk about. Having a public company hit a prime US stock market is another brick in the wall of “institutional credibility.”

🧠 And incredible for Circle. Like them or loathe them, they ground out a market share as a domestic, treasury-backed stablecoin.

🧠 Every global company is trying to figure out stablecoins. This week, the Uber CEO noted that while in the research phase, “stablecoins are very interesting for global companies.” Yes, they are. Corporate Treasury is about to get disrupted. SIBOS 2025 is gonna be electric.

🧠 This was a market mood test for IPOs, and the market said yes. Since tariffs hit a lot of companies backed away from IPO.

🧠How long til Chime and Klarna follows? Chime appears to be marching ahead. Klarna are primed and ready. We’re bringing much-needed liquidity back into the ecosystem.

🧠And how long til this IPO window closes? Business sentiment is down, demand for US Treasuries is down, and job losses are sweeping through the Fortune 500. We might get a few big GDP prints, but there’s also some flashing red signals.

Wise will move to a dual listing structure, maintaining a secondary hub in the UK, allowing Wise stock to trade on “a US stock exchange” and the UK. Wise reported revenue up 15% YoY to $1.6 billion, and profit up 18% to $564m (conversion accurate as of 5th June)

🧠 A sensible move for Wise.

US stocks generally trade higher than UK counterparts, with companies like ARM choosing the US for this reason.

This move also follows comments from the Revolut CEO that listing in the UK would be a failure in his duty to shareholders.

We also saw Darktrace be acquired by a PE firm, only to be floated in the US less than 2 years later for a major increase in valuation.

🧠 A massive blow to the UK. The UK government and London Stock Exchange has put massive effort into courting listings, changing its rules and bringing pension funds into the investment ecosystem more deeply.

🧠Quietly impressive growth continues.

Wise has three major customer segments all steadily growing, consumer, SMB and infrastructure.

That 3rd one could become a super power.

As they become the global money mover for banks, they’re perfectly setup to help the entire market move to new payments rails (like, I dunno, maybe, stablecoins? This is conjecture on my part).

Revenue up 48% to £1.2bn ($1.6bn), 67% of customers via word of mouth, up 25% YoY (!) Deposits up 48% to £16.6bn, total of 12m customers (up 2.4m YoY), 1m customers now use subscriptions (up 50%), 28% increase in weekly active customers to 6.4m.

🧠 These numbers prove they can cross-sell to the existing base.

Their attach rates are solid and improving driving up profitability

This is NOT damaging NPS or word of mouth

They have a sustainable advantage in low-cost customer acquisition

🧠My personal favorite thing about this company?

They're still the case study in product innovation

Their safety features prove UX in banking is not done

There's still a long way to go

🧠 If I have a worry it's this...

These numbers are still UK-centric

How many more years can they add 2+m customers?

They're yet to nail a second home market

Can they be the nice UK bank, or are they a global powerhouse?

🧠 The Chime comparison: Similar revenue, very different economics and products

They're in the same revenue ballpark ($1.6bn) but Monzo is much more profitable

Chime is targeting an $11bn valuation, says the latest headlines

Monzo has a charter, and is focused on whole market not subprime

They have a similar mission about transparency and fairness but don't mind fees

Monzo may not look to IPO til 2026, and in the UK

But if they did, which would you rather be?

🧠 If Monzo ever DID crack Europe or the US, they'd be a force to reckon with. They're still by far, the benchmark in terms of customer experience IMO.I regularly recommend to product leaders in other Geo's "copy + paste what Monzo did here..." and they do!

Tweets of the week 🕊

That's all, folks. 👋

Remember, if you're enjoying this content, please do tell all your fintech friends to check it out and hit the subscribe button :)

Want more? I also run the Tokenized podcast and newsletter.

(1) All content and views expressed here are the authors' personal opinions and do not reflect the views of any of their employers or employees.

(2) All companies or assets mentioned by the author in which the author has a personal and/or financial interest are denoted with a *. None of the above constitutes investment advice, and you should seek independent advice before making any investment decisions.

(3) Any companies mentioned are top of mind and used for illustrative purposes only.

(4) A team of researchers has not rigorously fact-checked this. Please don't take it as gospel—strong opinions weakly held

(5) Citations may be missing, and I’ve done my best to cite, but I will always aim to update and correct the live version where possible. If I cited you and got the referencing wrong, please reach out