- Fintech Brainfood

- Posts

- Wallet Wars: The Battle for Your Digital Life

Wallet Wars: The Battle for Your Digital Life

Digital Identity is about to reshape finance. It's finally happening. Plus; Election analysis for Fintech, why Affirm launched in the UK.

Simon Taylor

November 10, 2024

Welcome to Fintech Brainfood, the weekly deep dive into Fintech news, events, and analysis. You can subscribe by hitting the button below, and you can get in touch by hitting reply to the email (or subscribing then replying)

Hey Fintech Nerds 👋

How are you doing?

In other news. Fintech is on a tear.

Square, Visa, and Robinhood are all up big. The view is that de-regulation is a tailwind, and it possibly is. But if Square can match PayPal’s execution, Visa can get into Open Finance, and Robinhood can stick the landing on its new Stablecoin. The market is about to get reshaped again.

This week, Wise’s news of a 55% profit bump and a partnership with Standard Chartered shows an industry that is mainstream and delivers. Consumer-grade FX is now a Fintech specialty.

Never a dull week in Fintech.

Here's this week's Brainfood in summary

📣 Rant: Wallet Wars: The Battle for Your Digital Life

💸 4 Fintech Companies:

Astrada.co - Bring your own card as a service

Parlay Finance - AI Loan Intelligence System

Paydock - Payments orchestration as a service

Unit Plus - Treasury Management for German companies

👀 Things to Know:

1. Election bump for Fintech, Banks and Crypto

📚 Good Read: Fintech meets Telecom with eSIMs

If your email client clips some of this newsletter click below to see the rest

Weekly Rant 📣

Wallet Wars: The Battle for Your Digital Life

While everyone's watching AI, the biggest tech companies are quietly fighting for control of your digital identity. Apple owns 51% of the US smartphone market and just opened their NFC. PayPal is pushing Fastlane, Venmo, and partnerships. The banks launched Paze.

Wallet Wars in Finance and the paths to winning

This isn't about payments.

It's about who owns your digital future.

The wallet will become the consumers' center of gravity, not the account, app, or checkout. Consumers have countless cards, apps, and accounts that will be bundled by a handful of market actors like Apple, PayPal, Cash App, and possibly even Paze. But there are a lot of challenges to overcome first.

A decade ago, card issuers talked about being "top of wallet." Now, it's about being the wallet itself. Whoever owns identity wins.

The time is now. After an explosion of unbundling the banks, we're about to witness the great rebundling of financial services.

The crucial moment in the wallet wars was when the European Commission forced Apple to open NFC access to its devices, and now Apple has followed suit in many of its major markets.

NFC unlocks tap-to-pay, tap-to-enter (ticketing), tap-to-prove identity, and tap-to-anything.

Wallets will begin the great rebundling of finance.

Welcome to the wallet wars.

In this piece:

The great unbundling of financial services and the nightmare of fragmentation

The enabling technologies

Why owning identity is the core of any wallet

The routes market actors are taking to become wallets

Who has a right to play and who has a right to win?

The Great Fragmentation of Finance and Identity.

There's a classic image of the Wells Fargo homepage with arrows of 100s of Startups attacking each individual product and solution.

CB Insights Canonical Unbundling of a Bank image

This was just the beginning. Now we're entering the great rebundling. Why?

In the decade since that image became popular, thousands of consumer apps have launched, reached scale, and changed how consumers use financial services. Innovations like digital onboarding, cashflow underwriting, and mobile-only have created countless Unicorns, Decacorns, and a handful of Centacorns.

Wells Fargo is still very much alive, but there is no question that it's not the only choice for consumers.

In fact, consumers have too much choice.

The consumer app landscape is now so fragmented that it's become a bit of a nightmare. Despite the arrival of open finance and the promise of aggregating every account, there isn't yet a clear central hub for finance. Consumers might have a mortgage with one lender, a car loan with another, a checking account, a Neobank, a brokerage, or maybe even a side hustle with a business.

Then there are credit cards, airline cards, and rewards cards.

This fragmentation is a nightmare whenever you try to do taxes or admin.

You'll see the design target inside a classic leather wallet. It likely has a photo ID, a handful of cards, some loyalty points, and maybe even an event ticket stub.

Digital has hundreds of IDs, passwords, and subscriptions. The reality of the digital world is that there are now hundreds of online accounts, such as your email, subscriptions, social media, and others, for which you need passwords (or passkeys).

The idealized experience is the one wallet to rule them all and you can see it starting to happen. This wallet would have a strong, government-issued identity. It would offer all payment types, aggregate all your accounts, and help you optimize your finances. We're some way from this dream, but we can see early signs of what it might look like in Apple Pay, Curve, and Kudos.

Apple Pay is becoming the canonical wallet and payment button. handles airline tickets, event tickets, multiple credit and debit cards, and driver's licenses. It has a rapid checkout and embeds BNPL in the experience.

Curve aggregates cards and maximises rewards. Power users love solutions like Curve, which allow them to maximize their air miles and have lower FX fees. It also pioneered selecting the right card at checkout to maximize benefits.

Kudos is a Chrome extension that selects a card at checkout to maximize your rewards. It solves the issue of probably having a reward but forgetting existed or just not wanting to go through the admin headache.

(There's countless others I could name here, but the idea is to show the sort of roadmap potential)

Why Identity is the Key.

Wallets are the Everything app.

A wallet aims to combine multiple payment methods, ticketing, and identity into a single application. It can then be used for a variety of use cases. This idea isn't new. It has been common in Asia for a little over a decade. Apps like WeChat and Ali manage everything from a doctor's visit to your mortgage, payments, banking, travel, and work with national identity systems.

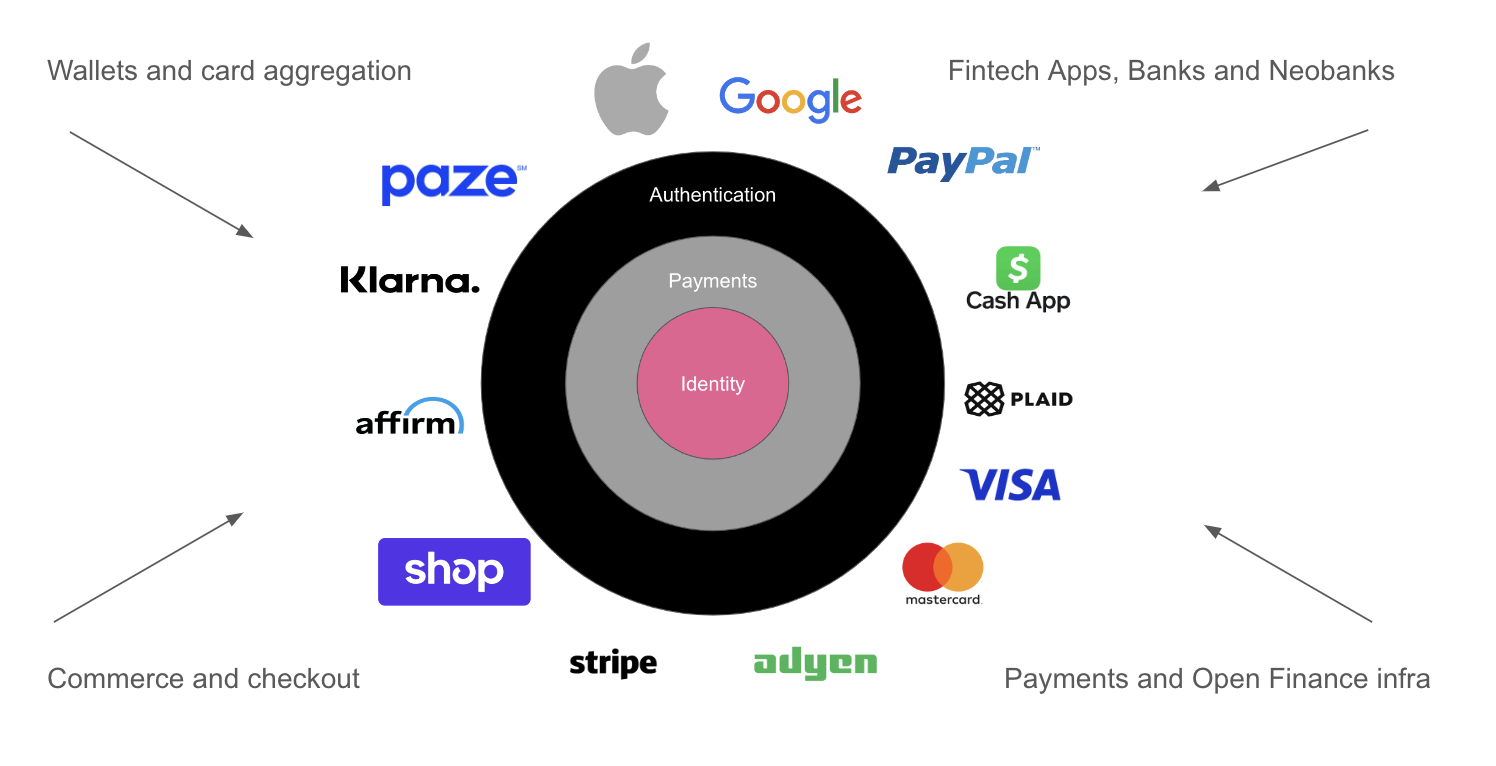

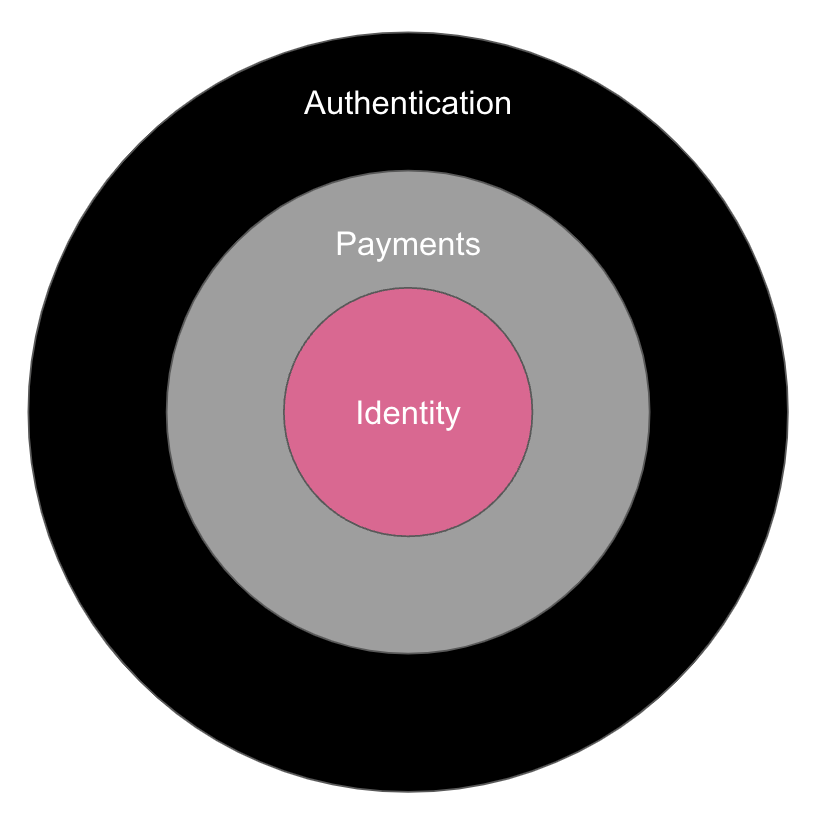

Identity is the core of any wallet

There are three core components to a wallet.

Authentication and Authorization: Airline tickets, concert tickets, stadium entry, bar entry, proof of age, tap-to-pay. The more tickets, payment terminals and access points a wallet can accept and authenticate to the better.

Payment methods: Credit cards, debit cards, Pay by Bank, International, and countless payment rails. The more rails in a single wallet, the better. This creates a "super rail" that operates as a branded checkout (like Apple Pay), but can use any payment type (e.g. BNPL, cards)

Identity: A standardized, tamper-proof government-issued identity (like a passport or driver's license). Real ID will come with an application that can manage identity; it can easily do anything else.

What's powerful is that now:

The US Government, with Real-ID, has a standard that any wallet can use to obtain a cryptographically secure (PKI) signed identity from a state agency like the DMV.

Multiple payment methods now exist in a single wallet, with Apple Pay supporting credit cards, debit cards, BNPL and even P2P. Accelerated Checkouts are also becoming compatible with those wallets.

Acceptance for NFC authentication at stadiums, venues and bars is now becoming much more common in the US. Services like CLEAR make face ID and strong biometrics even more widely accepted.

As digital identity expert Jamie Smith explains, the wallet goes way beyond just storing payment methods:

My view is that 'digital wallet' just means 'cryptographically provable'. They can store whatever data is needed. Meaning it will come down to context, brand and relationship.

The tech enables various brands, contexts, and relationships to move towards becoming wallets. Which brand? Which context? Understanding these is the key to understanding how finance will be bundled.

The user and ecosystem is ready for wallets that do more.

Market shifts happen when the market is ready to accept a change. In the past decade, digital identity, tap-to-pay, and new payment methods have become conveniences users enjoy.

These can now be embedded in any wallet.

a) Tap-to-pay and tap-to-enter are well-understood UXs, and NFC is now open. We've had cards in wallets for a decade or so. Tap-to-pay and tap-to-enter a stadium are now common user experiences in the US, UK, Australia, and Europe. Stadiums are especially NFC-friendly in the US. Apple's recent decision to make the NFC chip more open is a game-changer, given that they have a 51% smartphone market share in the US.

💡 Wallets connect these experiences in a single UI. Apple Wallet is one approach, but now there's an opportunity for any company to become its users' default wallet for identity, ticketing, or payments.

b) Pay by Bank changes the economics of payments for wallets. Historically, peer-to-peer communication was expensive and slow. In the US, it's still common to rage-quit and send someone a check because paying by Bank was so hard. Countless Fintech companies wedge product was a closed loop P2P capability (Cash App, Venmo). Modern Pay by Bank, where a user authenticates using an open finance flow (like Plaid or Truelayer), is far simpler for P2P, large payments, or even e-commerce checkout. It's also often cheaper for the payment provider.

💡 Putting modern Pay by Bank in a wallet gives wallets a killer app. It opens new use cases like P2P or higher-value payments. At e-commerce or recurring payments, we also see merchants fund incentives like discounts to encourage Pay by Bank usage.

c) Digital Identity technology changes the payment experience. In Estonia if you hit checkout during e-commerce, you can use your Smart-ID (mobile app identity) to approve a payment. This is a much stronger authentication than a card-not-present transaction. It also makes other payment rails (like Pay by Bank) more appealing and easier to use.

💡 The USG has started providing digital identity standards (Real-ID). Apple Wallet has a lead here, but any wallet could use this standard.

Let that sink in.

Consumers love accelerated checkouts and BNPL.

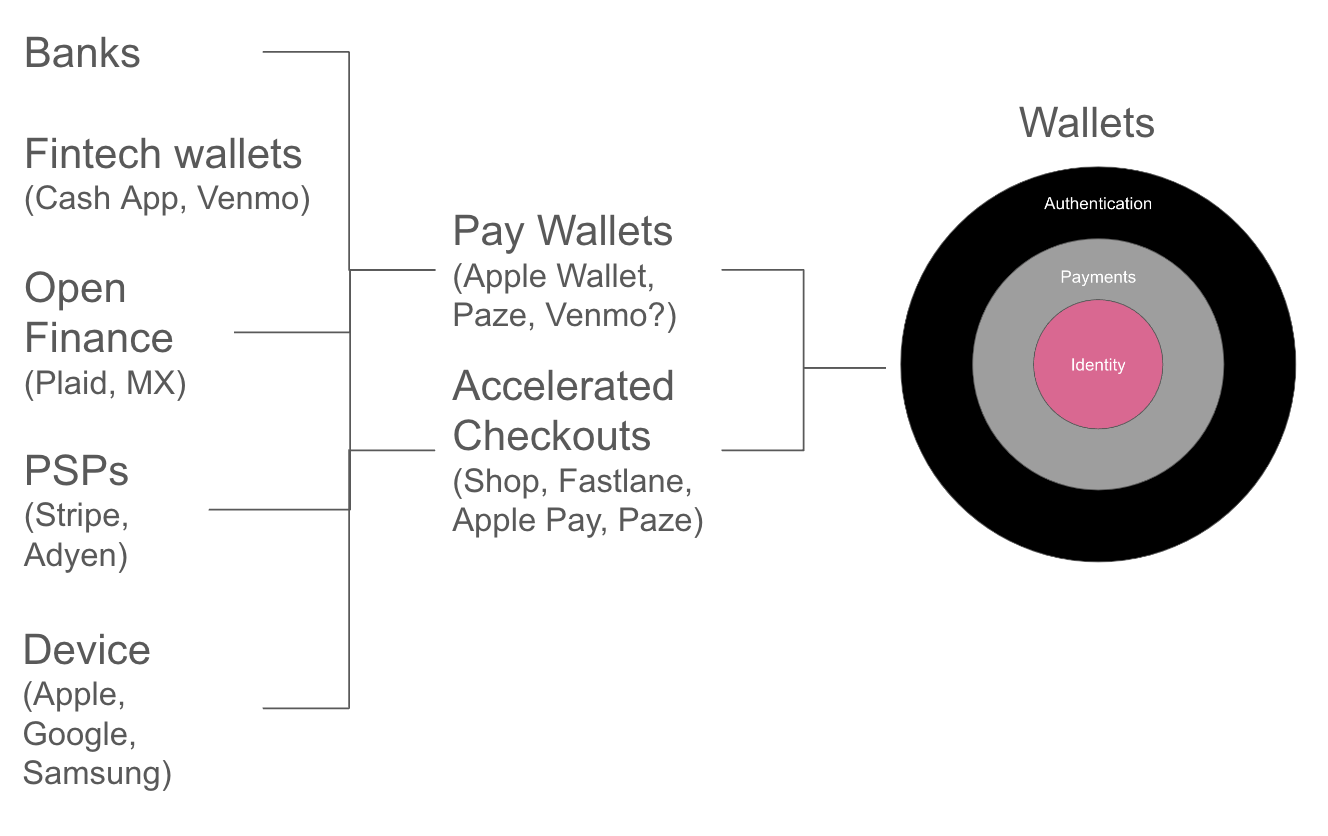

The Five Paths to Victory

There are five paths to becoming a winning wallet that roll up into two “wedge areas”:

Leverage identity assets to become a consumer finance (pay) wallet

Leverage accelerated checkouts to become a consumer commerce (checkout) wallet

The Five Paths Finance companies have to try to own Identity

Getting to "own" the user identity depends on who can provide the most utility. For payments specifically, there are a handful of actors with a claim.

Each brand has a different relationship with its users and can win in different user contexts (like pay, approve, prove I'm over 18, etc.) given its access to devices or identity.

Let's look at who's taking each path, and their chances of success:

OEMs and device manufacturers can use hardware to secure wallets. Apple used its walled garden to gain a massive market share lead for Apple Wallet under the guise of security. Google and Samsung have followed suite. Samsung Pay+ is a card that aggregates other cards.

Banks have cards and potentially a solution in Paze to become wallets. The banks have many possible paths. Visa offers the Visa Flexibile credential and click-to-pay solutions to offer accelerated checkout-like experiences from any card and even support Pay by Bank. Paze also provides a brand to become a multi-bank wallet.

PSPs like Stripe and PayPal offer their own accelerated checkouts. Stripe even offers a consumer app that connects paying and checkout. Shop Pay also has both the consumer app and the branded checkout. What differentiates these solutions is they often go deeper into managing experiences like delivery notifications and improve conversion at checkout by removing clicks. To some extent, BNPL payment buttons and apps fit this category, too.

Open Finance providers provide a new payment rail and identity assurance. Pay by Bank is now a card-like experience at checkout. A user can click to pay and authenticate by linking their bank account. In the US, storing that credential like a card on file or an "account on file" so future payments become one click is possible. Because the authentication comes from the Bank, some identity "proof" also comes with the transaction flow. Open finance providers may end up tucking behind the PSPs, but they may also become an identity wallet in their own right.

Fintech Wallets are well placed to become wallets, and now NFC is an option. Venmo and Cash App had largely stagnated in the past decade, having gone about as far as the payment rails allowed. With NFC opening and Pay by Bank coming to market, perhaps they can start to bring more of a holistic offering together. They have some element of identity but don't play in ticketing.

BNPL apps are becoming wallet-like. Affirm and Klarna have shopping apps, send goods delivery notifications, and offer a payment button at checkout. They're integrated with multiple PSPs and appear in wallets like Apple Pay, but they're yet to take on any larger role in identity or ticketing.

So, the remaining question now is what happens now? Everyone wants to use their wedge to ultimately own identity, but how they get there may vary.

Who will win?

Jamie Smith put it brilliantly while I was researching this piece.

1. Which wallet has a right to be the center of gravity?

With payments we can store 'proof of money/account'. With digital ID wallets we can store 'proof of attributes' (personal data). We're going to see wallets everywhere, and will use multiple wallets daily (health, money, travel, government).

2. Which brand has a right to be the wallet?

Would I add my boarding pass to my bank app? Would I add proof of salary to my airline app? No. We'll need new wallet brands. But we'll also need to authenticate to ALL of them (is this the right person or agent accessing this wallet). Most likely, digital wallets will be abstracted away from the customer experience.

3. The best customer experience is NO customer experience?

Today I tap to pay. Tomorrow I will 'tap to pay plus ID attribute' (e.g. >18, VIP etc.). Soon my AI agent will handle those specific transactions, and I will just say, 'Check me in,' or 'Apply for the role.'

Here's how I think it plays out:

Apple has 51% smartphone market share, identity + wallets + hardware + local AI, but lost its mojo and pace. OEM wallets can do strong identity, ticketing and payment methods. They're also becoming accelerated checkouts and can bake agents into the device. Apple is in the lead and has all the tailwinds, but it is also moving slowly. Yet, Apple may have lost its mojo.

Banks and Paze will follow, not lead the market. I doubt they’ll do much with “AI agents”. They'll have scale and instant distribution, but they won't imagine the future. The Venmos and Cash Apps of the world have a generational opportunity to build something truly magical for their customer base.

PSPs can become the ultimate aggregation point. Stripe Link is fascinating. If you model it out, Stripe Link is a consumer wallet, but Stripe can support open finance, Visa flexible credentials, BNPL, and offer various accelerated checkout solutions. Expect Adyen to follow closely.

Open Finance has a claim at identity and aggregation but is probably more of a data provider. Plaid, in particular, is a strong consumer brand, but in time, "account ID" or Tokenized Account Numbers (TANs) start to resemble tokenized card numbers (DPANs). Open finance is ultimately infrastructure, not consumer.

Fintech wallets like Venmo and Cash App have a generational opportunity. They could innovate with AI Agent-like experiences. PayPal with 400m users, merchants, and now Fastlane and some Mojo is playing to win. Flexible credentials, tokenized accounts, and open access to NFC are a gift. If they can get a strong identity right, they can start to aggregate multiple services without providing them all in-house. Your wallet could be more of a marketplace and less of a store.

Accelerated checkouts provide convenience but need to become wallets. They're almost the perfect wedge for commerce and user adoption, but they're yet to bundle loyalty or identity well. Klarna and Affirm probably fit better in a wallet than existing as a wallet.

None of these players will disappear, all of them will continue to be in the landscape. But the prize? The prize is bigger than that.

The Prize: The Everything Wallet

The Everything wallet: A wallet that combines identity, payments, and tap-to-anything will own the future consumer experience. There are many paths to becoming that wallet, but the prize is truly owning a customer in a way that wasn’t possible for the universal banks.

The players: OEMs, Fintech Apps and Banks have all started towards becoming an everything wallet. The OEMs are closer to identity, but with NFC available now its open season. The card networks, open finance companies and PSPs all have a path to more market share as infrastructure for identity in wallets.

The Everything Wallet will

Own a strong identity credential backed by a Government entity

Aggregate all of my accounts, tickets, and loyalty

Route my payments by highest points or lowest cost

Manage delivery and returns elegantly

Help me find new products

Automagic away admin like taxes or refunds

Support stocks, investments, and savings and manage sweeps

Natively support stablecoin and cross-border rails (there’s an entire Rant about why for another day)

People don't want to manage their money; they want software to do that for them.

In the next 12 to 24 months, watch as Fintech companies, banks, and Tech companies go after identity and payment methods much more aggressively.

The battle for who gets to BE the wallet is on.

Let the wallet wars begin,

ST.

PS. I didn’t even start to cover CLEAR, Crypto wallets, and where AI Agents fit in all of this. Unpacking that would be a book.

🧠 If Fintech Brainfood did a training course, what should it be about? I get asked to do this a lot, so I've put together a survey. I'd love your thoughts. Give this link a click. It will take 30 seconds, and your answers will help me massively 🙏

4 Fintech Companies 💸

1. Astrada.co - Bring your own card as a service

Astrada helps platforms and marketplaces build embedded finance experiences (like travel, payroll, or payouts), and users get to keep their existing cards. Users benefit from their existing rewards or points program, and marketplaces get to run "embedded finance" without getting in to issuing their users with a new card.

🧠 This reminds me of how Navan pivoted to BYOC and stopped issuing their own card. It allows them to expand their partnerships potential, but still give users that embedded travel experience. The SaaS is increasingly embedded, and the card experience is a little more hidden and streamlined. This is very cool. If Shopify offered this, instead of getting a Shopify Balance card, you'd use your existing card with Shopify, but it still has all the same features.

2. Parlay Finance - AI Loan Intelligence System

Parlay Finance sits alongside a lenders Loan Origination System (LOS) to provide simpler applicant UIs, a readiness forecast, and analytics to help improve pipeline efficiency.

🧠 This is digital transformation in a box: a new front end and the data and dashboards to power more lending within risk appetite. For most, underwriting is still a world of spreadsheets and committees. Parlay is aimed squarely at community institutions that don't have a large digital transformation budget.

3. Paydock - Payments orchestration as a service

Paydock is a whitelabelled orchestration platform for acquiring banks. It helps those banks fight back against new players like Adyen and Stripe by giving them the best of modern developer experiences and merchant solutions over their legacy stack. Merchants get access to multiple gateways, providers and value added services

🧠 The legacy acquirers can no longer compete on price alone. Paydock can potentially upgrade their tech, and offer merchants maximum flexibility without the massive internal transformation. It also means they could de-risk any new system setup under the hood. Merchants would get the same API endpoints while acquirers can test their old and new services side-by-side. This "cores side-by-side" is now widely understood to be best practice.

4. Unit Plus - Treasury Management for German companies

Unit Plus offers 3.68% yield credited daily to help companies optimize working capital. It offers instant deposits and withdrawals to a Goldman Sachs money market fund. The service also calculates realized and unrealized gains in an accounting software-friendly output. They also publish this interesting index on interest rates for overnight funding solutions.

🧠 German companies need treasury management too. I love the idea of publishing an index as a way to drive industry transparency and competitive advantage. It's the kind of sales approach that says "hey I've done the homework for you - here's the right answer - its us."

Things to know 👀

1. Election bump for Fintech, Banks and Crypto

In the first full day of trading since the US election major US banks such as JP Morgan, Wells Fargo and Citi (8.4%) all traded up significantly. Meanwhile, Robinhood (19%), Coinbase (31%), and Block (7%) all rocketed (vs the S&P up 2.5%)

🧠 No Basel III Endgame could be Christmas early for the banks. Basel III would require banks to hold 9% more capital, potentially making them less profitable (they already watered that down from 19%). If there’s one thing the banks cannot stand, it’s the idea of being less profitable due to regulation—something Jamie Dimon has been incredibly outspoken about. Maybe now it goes away entirely.

🧠 Crypto and correlated stocks are up big. Bitcoin jumped nearly 10% to an all-time high, and Coinbase and Robinhood also benefitted. The Senate Banking Committee chair lost their seat in the election, and Trump has promised to displace the SEC Commissioner. For me, that’s beside the point. We’ll get regulatory clarity in the next administration, and that alone is worthwhile (and a net positive for consumers overall).

🧠 Fintech still has great fundamentals: high rates and high digital adoption following the pandemic. Add to that possible deregulation, and we’re in good shape. But I do worry we’ll fail to learn the lessons of the last two years: consumer harm, bankruptcy, and ledgers that don’t add up. This is the stuff of nightmares. Let’s build better.

🧠 There’s still a consumer struggling to make ends meet. A big motivator for the election was the cost-of-living and high prices. AKA, inflation. We have a hollowed-out middle class who feels unheard and unsupported. Everything costs too much. The answer can’t be more debt. It has to be better finance. Finance accelerated.

🧠 We’re not in ZIRP but this already feels frothy in the midst the AI bubble. Stocks are way overvalued compared to historical averages. If tariffs bite, if inflation hits hard, this could get ugly.

The largest and most well-known BNPL provider said it has hired 30 local staff and announced its first clients Fexco and Alternative Airlines.

🧠 Why launch in the UK? It's an English-speaking market, where some large existing clients like Amazon and Shopify have significant market presence. It's a no-brainer.

🧠 Competition for Klarna. The UK is one of Klarna's largest and most lucrative markets. Klarna announced late fees this year, while Affirm is promising "no hidden fees" to differentiate.

🧠 UK Expansion is all the rage with US Fintech. Robinhood and Affirm have both launched recently, and Square is hiring and expanding its product team dramatically too.

🧠 Affirm has done well with offline merchants, could it do that in the UK? We don't see much BNPL in-stores here. While Klarna is entrenched in e-commerce, they haven't gotten far at the point of sale.

Good Reads 📚

Nubank, Revolut and Bunq have all launched "Telco like" services by providing eSIMs to their customers. Telco's have been trying to enter finance for decades with success in emerging markets, but poor results in the profitable developed markets. eSIM's allow a new mobile operator to be downloaded directly to your smartphone (via providers like Gigs).

🧠 Understanding eSIMs - the embedded Telco. eSIMs are to Telco's as BaaS is to banks. Gigs, Mobilise and Better roaming offer simple APIs to embed the SIM provision in finance and non-financial brands.

🧠 Historically this was helpful for travellers, but it's becoming a business model for Fintech. eSIMs are a new way to drive revenue, and they're super valuable for travellers. If you're a brand used by travellers like Revolut, it's a logical product extension.

🧠 What's the subscription model for digital banks? Bank subscriptions suck. Packaged accounts usually have terrible products with high breakage (they're profitable if people don't use the benefits). The twist now is to build products people might actually use. What a wild idea.

Tweets of the week 🕊

eBay executed a savvy deal in Jan 2018 by negotiating warrants equal to 5% of Adyen in connection with their processing deal. eBay just executed the 2nd tranche of 1.25% at €240 per share (current market price is ~€1400). 5% of Adyen is ~€2.15B. adyen.com/press-and-medi…

— Scott Wessman (@scottew)

10:51 PM • Nov 4, 2024

That's all, folks. 👋

Remember, if you're enjoying this content, please do tell all your fintech friends to check it out and hit the subscribe button :)

(1) All content and views expressed here are the authors' personal opinions and do not reflect the views of any of their employers or employees.

(2) All companies or assets mentioned by the author in which the author has a personal and/or financial interest are denoted with a *. None of the above constitutes investment advice, and you should seek independent advice before making any investment decisions.

(3) Any companies mentioned are top of mind and used for illustrative purposes only.

(4) A team of researchers has not rigorously fact-checked this. Please don't take it as gospel—strong opinions weakly held

(5) Citations may be missing, and I've done my best to cite, but I will always aim to update and correct the live version where possible. If I cited you and got the referencing wrong, please reach out