Hey Fintech Nerds 👋

Heads up, I’m about to take a two week break from Fintech Brainfood. I have a family vacation coming up and a lot of day job to catch up on.

I had a conversation this week where someone went, “Oh, so blockchain networks are like the FBO account.” And, kinda. But there’s so much more here.

Stablecoins are not just another rail; they’re a new way to build financial products, with differentiated economics. This week’s Rant is a side-by-side comparison of the BaaS stack and stablecoin stack.

See you in two weeks 🙏

Here's this week's Brainfood in summary

📣 Rant: Stablecoins are a Platform pt3

💸 4 Fintech Companies:

Polar - Complex Billing for AI Agents

Nevermined - Complex Billing for AI Agents (snap!)

Ivy - The Global Pay by Bank Aggregator

NaroIQ - Whitelabel Fund infrastructure

👀 Things to Know:

Kalshi raises $185m at $2bn valuation. The Circle of Prediction Markets?

Want to support Fintech Brainfood? Get yourself to Fintech Nerdcon in Miami, or check out the work we do at Sardine*.

Weekly Rant 📣

Stablecoins are a platform pt 3 - The stablecoin stack.

Banking as a Service turned bank charters into APIs - what once required years and millions became weeks and 10s of thousands. Stablecoins let anyone build financial products with new lisenced entities (stablecoin issuers), and with instant settlement. When you remove fundamental constraints, once impossible business models become inevitable.

This rewrites the economics of building financial products

For example; Real-time lending. Today's credit card programs require securing facilities, managing settlement delays, and endless admin. With stablecoins, a customer swipes → funding pulls directly from your credit facility → settles with Visa instantly. All automated.

This post examines

Stablecoins are a platform

Who this platform shift impacts

The platform opportunity

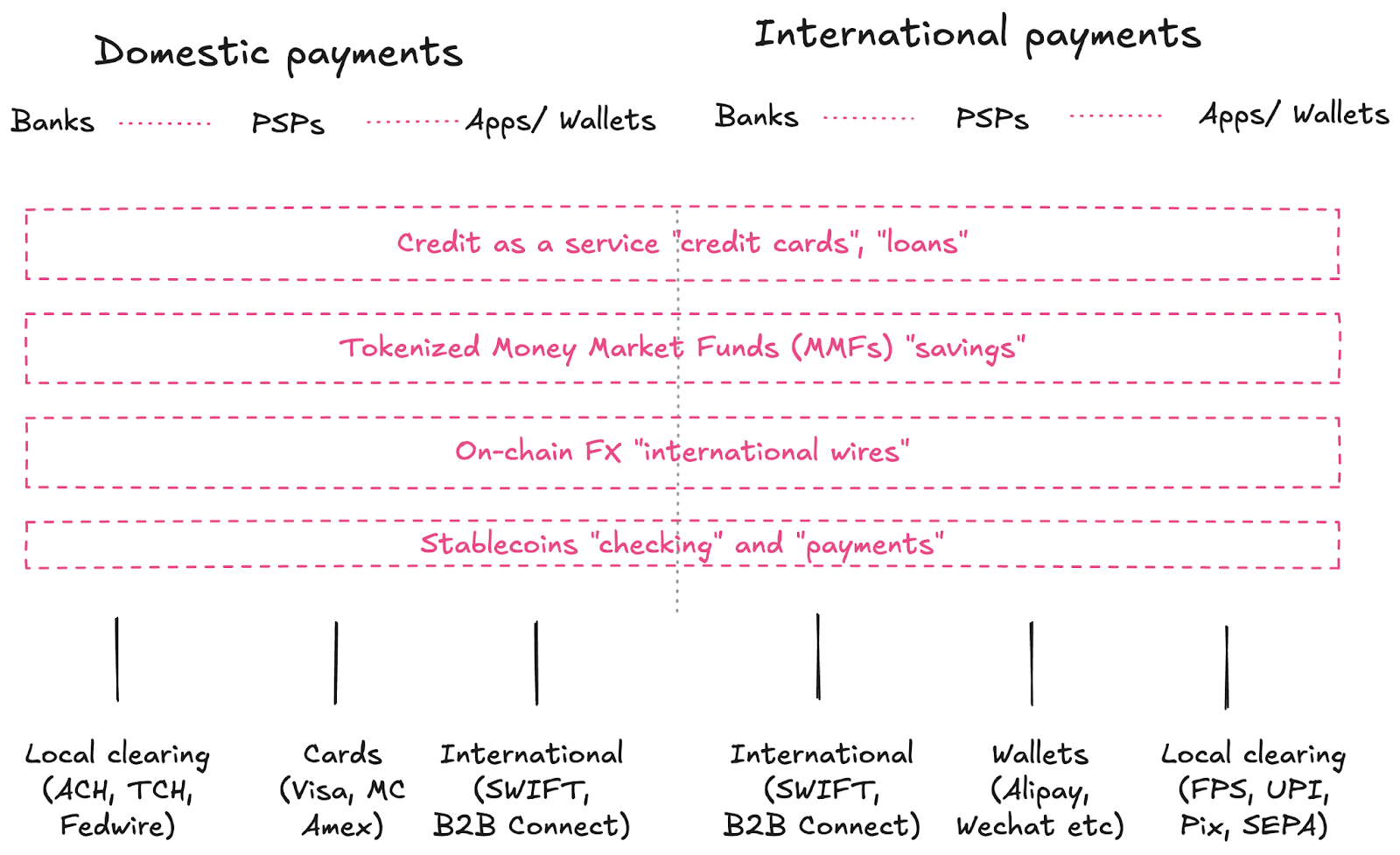

The BaaS stack

Where money lives in the BaaS stack

The stablecoin stack

Where money lives in the stablecoin stack

Your opportunity.

Stablecoins are a platform

Any financial product you could build on traditional rails can now be built on stablecoins and with onchain finance. But more importantly, the instant, programmable nature of stablecoins lets you build new products and experiences with new economics.

With real-time lending, as a non-bank card program, you could have a customer swipe a credit card, pull that funding directly from your credit facility, and have it settle with Visa instantly. You could also link the customer repayment to paying back the lender. All automatically. As the CEO of Rain explained on Tokenized recently.

Current fintech: You need cash upfront to offer credit

Stablecoin world: Credit facility becomes your real-time cash flow

That's was a holy sh*t moment for me - no more pre-funding credit programs

It’s not every day you see something genuinely new in payments. And this is just one example. The whole world of being a non-bank lender is about to get 100x more efficient and nobody is paying attention. (FWIW, Rain uses Fence Finance* for this capability, and if you’re in lending you should take a look at what they do).

If fintech changed the distribution of finance, onchain finance is disrupting the manufacturing of finance. You can build an entirely new business without needing a “core” ledger or “core” payments provider.

Everyone’s writing a strategy for a world that could be incredibly different in 12 months and trying to figure out what it means for them, the market and their portfolio.

What happens when settlement constraints disappear?

I’ve been invited to at least nine analyst calls this week (I only attended one, as Justin at UBS is a legend). Everyone wants to know who stablecoin “kills” since the Circle IPO spiked so high. And no doubt, stablecoins are disruptive, but we’re looking at the questions far too simplistically.

Does that mean cards are dead?

No. The fact that the Visa CEO had to go on CNBC and explain that, because Walmart and Amazon announced they are looking at stablecoins, tells you we’re at peak stablecoin hype and FUD.

Does that mean card processors are dead?

No. Card processors become the ISPs of the stablecoin era. They connect the security UX (a card in an Apple Wallet linked to a stablecoin)

Does that mean banks are dead?

No. We no longer need banks to manufacture or distribute finance. There’s a massive opportunity for private credit and shadow banks. But there’s also real space for specialist banks to be the worlds best on and off ramp. Just as specialists did well in the BaaS era, they could do 100x better in the stablecoin era, with more use cases and more potential client bases.

Is anyone dead?

No. Old finance infrastructure never really dies. It just erodes in relevance. New infrastructure can grow incredibly rapidly. And that’s the market opportunity. New products, new businesses. Things we couldn’t do before because they were too costly, or too risky.

The platform opportunity is much more than “just another rail”

If nobody dies who wins? That’s the right question. Yes, banks too could build those products, distribute their existing products and use stablecoins as “just another rail” but if that’s all you see, you’re missing the bigger shift. Stablecoins are a rail that is global, 24/7, instant and programmable. This means we can build new products, and entire companies on stablecoins.

The bank talking point is that “stablecoins are just another rail.” I can see why its tempting to say that, but its a misleading statement.

It undersells the opportunity. I get the need to make it “not a threat” and “just something we’ll do like Zelle.” But Zelle didn’t have an ecosystem of other financial products, or an asset class worth trillions, or shadow banks aggressively entering the market.

We have the biggest change to financial services regulation since Dodd Frank in 2010.

That means we have real competition for who gets to own the manufacture and distribution of finance across all customer segments.

To examine how, we have to contrast fintech products vs stablecoin products. Starting with a look back at fintech:

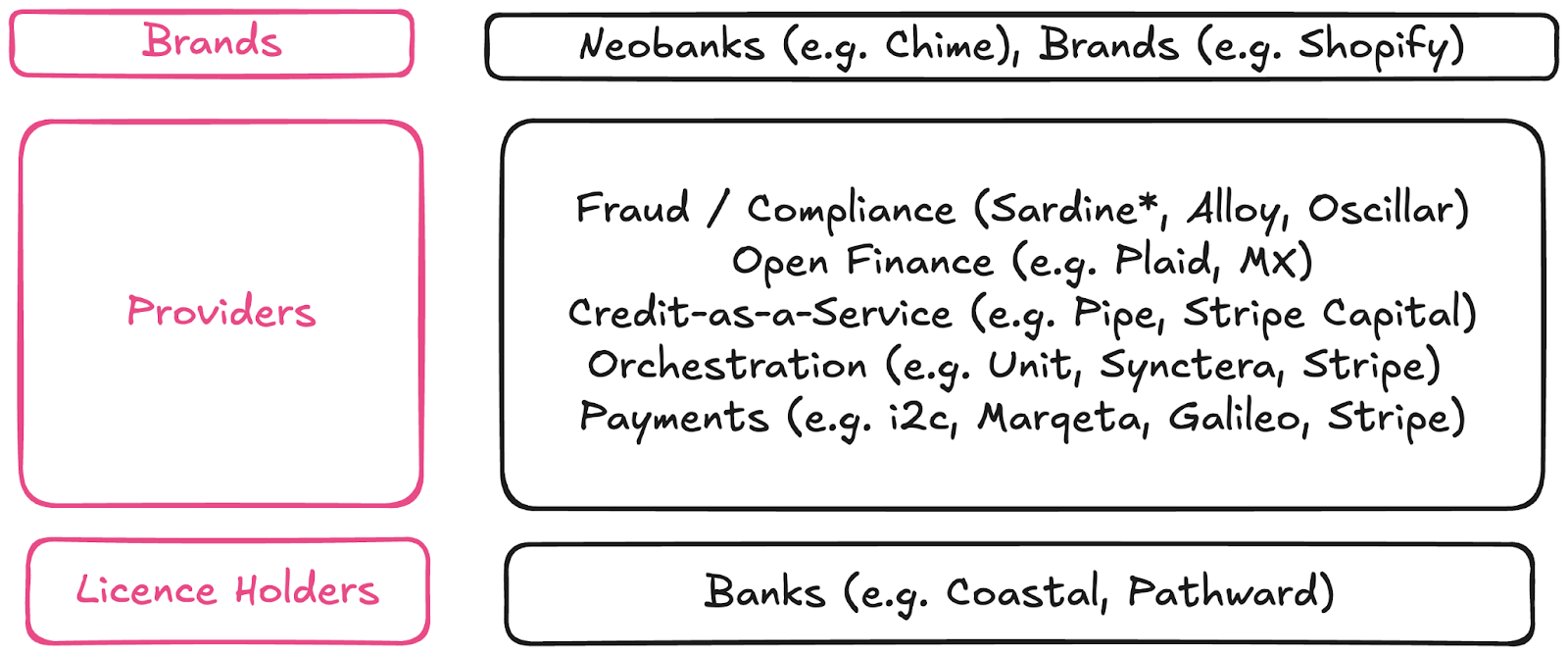

The Banking as a Service Model

In the 2010s “Banking as a Service” made it much easier and cheaper than ever to sell build a card program and launch an account for consumers. What was once a bank department became an API start-ups could quickly and cheaply adopt and integrate.

The BaaS stack that dominated the past decade is now very familiar

This allowed more non-bank brands to come to market.

Co-branded cards have existed for decades. However, the reality of your airline's reward card is that it’s essentially a bank product, featuring a bank website and a mobile app with the Delta or AA logo on everything. It was whitelabel, not “as a service.”

Getting here still required access to the banking and payments “rails” like cards, ACH and wire. This became an opportunity for the smaller banks who were able to “rent their charter” by partnering with 3rd parties (e.g., a Neobank). These Neobanks and non-banks who would then use the API providers assemble a customer-facing product.

BaaS removed licensing constraints but kept settlement constraints.

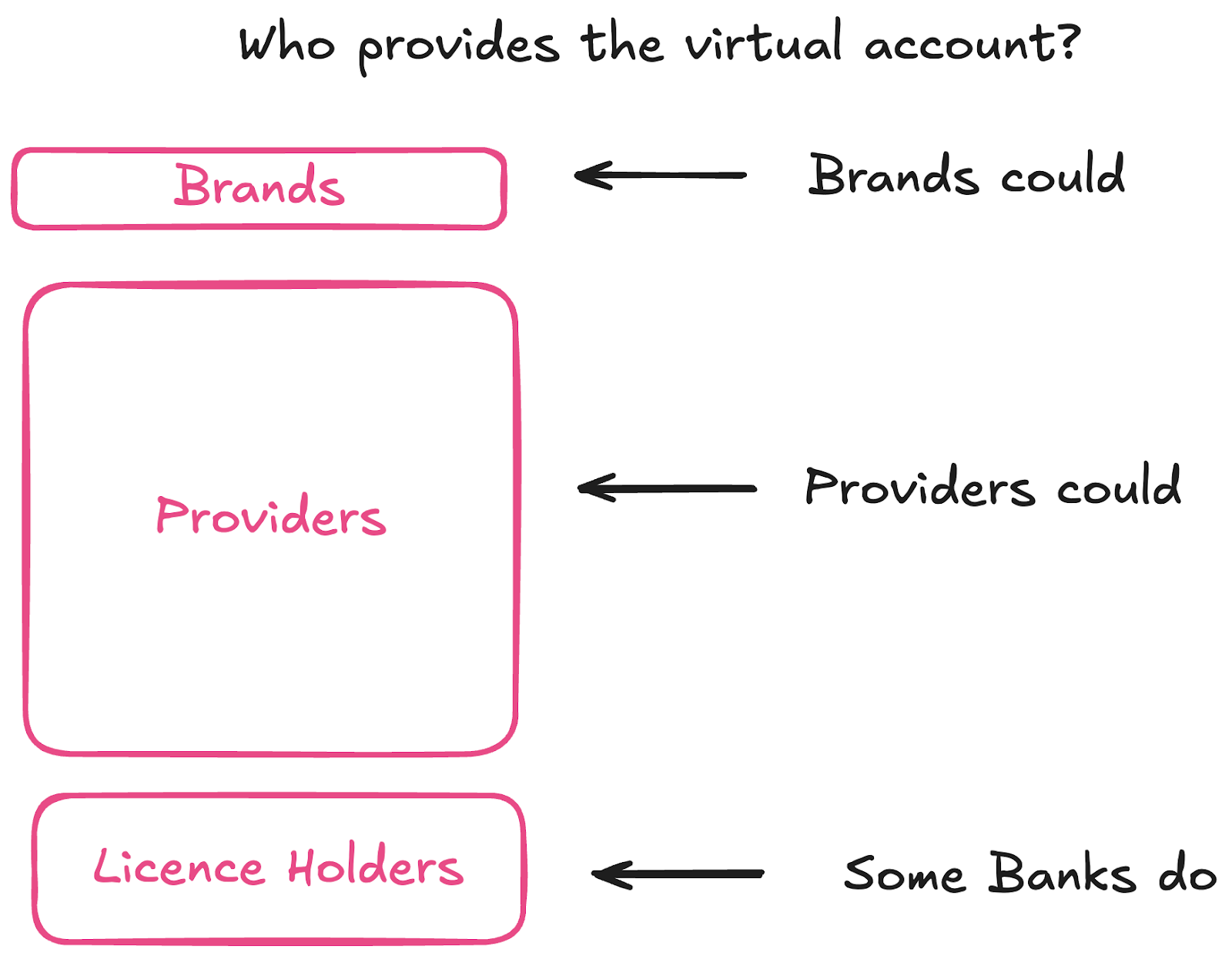

Where does the money sit in the BaaS model?

Money lives at a bank. In the BaaS model in the United States, people that’s historically lived in an “FBO” or For Benefit Of structure.

(Although many fintech companies graduate to getting their own, state-by-state money transmission licences, the FBO structure is often preferable, especially for non-finance brands. In Europe, many get EMI licences etc.)

At a high level, FBO accounts enable businesses to manage their clients’ money without the costly regulations that can come with certain types of money transmission.

If you move money for your customers, the FBO account is one giant account. If you have 1,000 customers' money, that all sits in one big account mingled together.

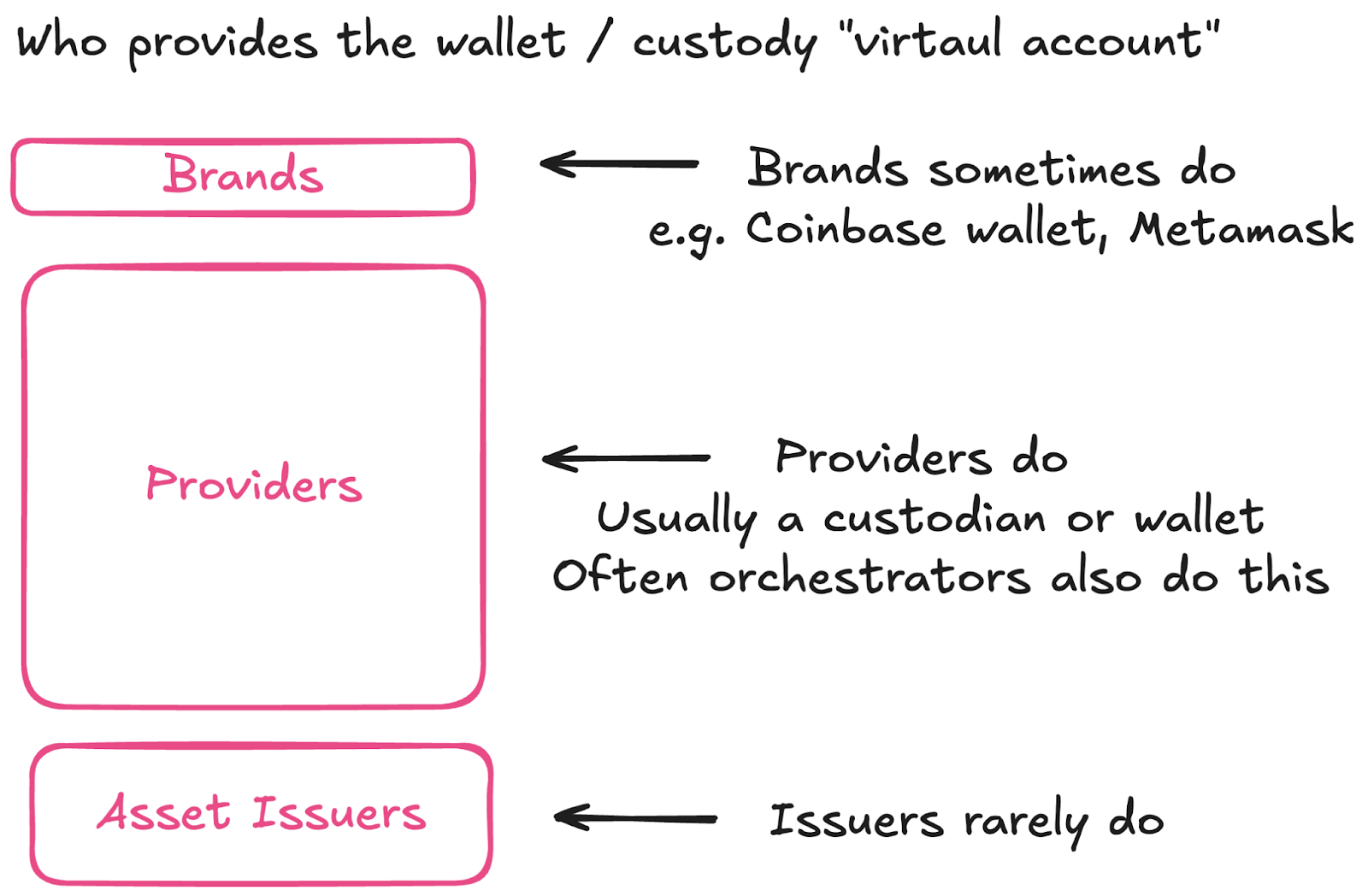

To solve that, you un-mingle it with sub-ledgering or “virtual accounts.” These can be built by the Neobank (as Chime has), offered by the provider (like the payments company), or sometimes, banks offer it as an additional service.

It’s not obvious who keeps track of customer funds in the BaaS model

The money legally sits in the FBO account. But the manager of the “virtual account” figures out which dollar belongs to who.

Confusing? Yes. Especially if the bank holding the FBO, and the sub-ledger provider can’t agree (reconcile) which account has which money. And that’s exactly what went wrong in the Synapse/Evolve disaster that left more than 100,000 customers without access to their funds.

Knowing where the money sits and who does what is key.

We’ve reached the limits of how much technology can transform the aging legacy infrastructure into something new. Stablecoins and the GENIUS Act represent the single largest new policy and regulatory development in financial services since Dodd-Frank of 2010.

You wait for decades to get a Fintech charter, and get a stablecoin bill instead.

The stablecoin financial products stack

Stablecoins are to banking what the internet was to telecommunications - not just better, but a completely different platform. While to a customer, modern stablecoin products often look like any other Neobank, they run on a parallel infrastructure. Whatsapp is a bit like SMS in core functionality, but a lot better in its experience.

(No metaphor is ever perfect but go with me here).

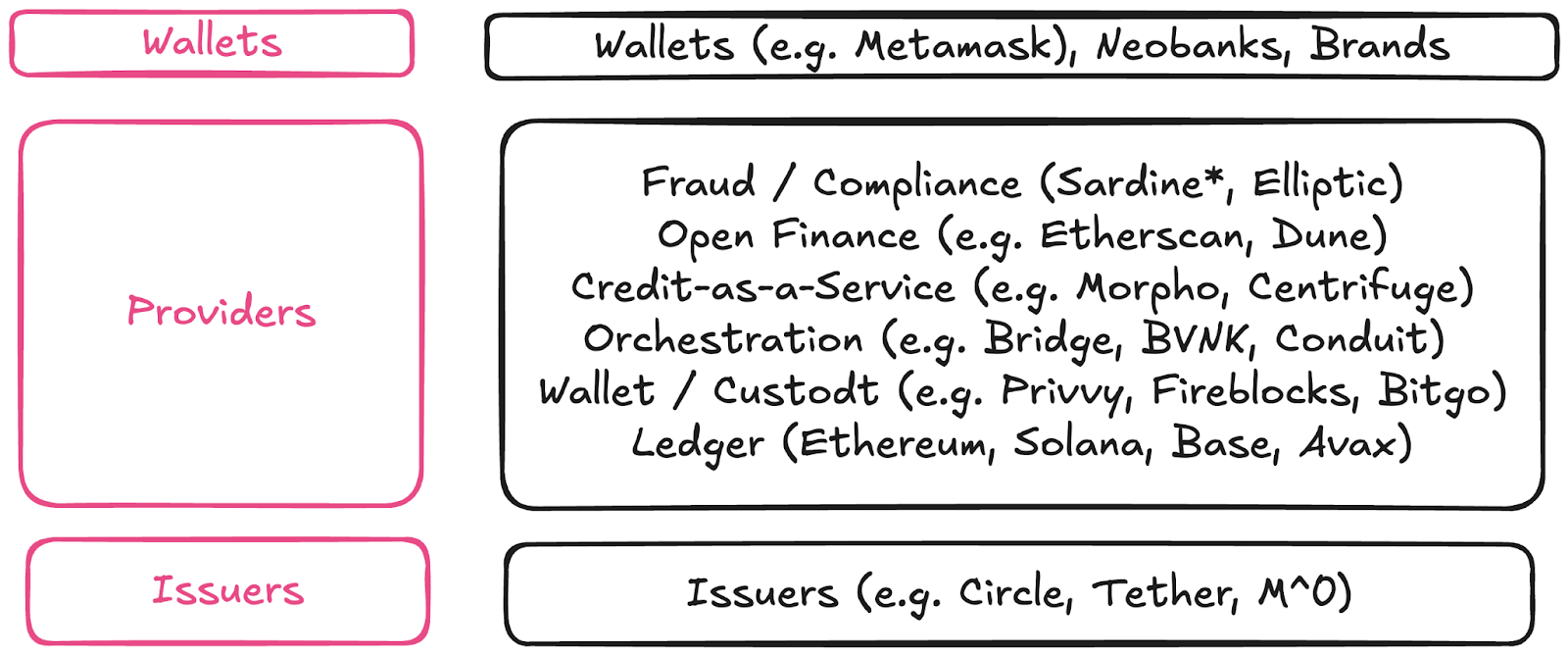

A simplified stablecoin stack

At the UX layer, “wallets” can be direct-to-customer apps, or they can exist inside a Neobank (e.g., Revolut, Cash App)

At the provider layer, there are a handful of major differences.

“Open Finance” is different because most transactions are on a public network.

The question is whether your app or interface is letting you use all of the native capability to access that ledger (like Phantom or Metamask would), or if they’re constrained experiences (like a Neobank might to limit the risk surface).

Credit-as-a-service is wildly different because it’s all private credit on defi rails.

This could ultimately become the most transformative part of the stack. Historically, DeFi was overcollateralized lending, not very efficient. That’s changed in a big way.

We’re entering an era of real-time lending. Today, as a non-bank credit card program, you have to secure a lending facility, draw down on it, so that customers can spend. You then have to manage mandates, legal documents and multiple accounts to pay all of that off. You’re paying higher fees, dealing with settlement delays and admin.

Orchestration hides a massive amount of complexity.

To work on stablecoin rails, you need to connect custody, wallets, multiple networks (Solana, Eth, Tron, Base), multiple stablecoin issuers (USDC, USDe), exchanges, OTC desks to the TradFi ecosystem. That means banks, payments companies, and the whole TradFi stack, and licensing, for both crypto and TradFi. Orchestrators solve a much bigger pain for, say, payroll platforms than traditional fintech orchestrators who solved “I don’t want to get MTLs or set up an FBO.” Crypto is at least 2x harder. At least today it is.

Custodians and wallets are the security engine of stablecoins. Self-custody wallets help you as a business or individual, manage your own stablecoins and assets. What makes Privvy (or Fireblocks Wallet-as-a-service) interesting is that it provides this capability as a headless service. So you, as a business, could hold stablecoins just like having a vault of cash, except it’s a vault you hire as an API. You stay out of the crypto funds flow, and users get all of the benefits of stables without necessarily knowing they're using them. In that model of self-custody, you do have the potential risk of securing the keys to your vault.

So, alternatively, a custodian can take care of all of that risk, but they too can make wallets “embedded” inside a Neobank or non-bank interface. Weirdly, custodians kinda map to payments companies, they’re where the instruction from the customer to move an asset is presented with keys, to the underlying network.

The ledger (e.g. Solana, Eth) is like an FBO account that reconciles itself. Unlike banks that control your account, blockchains don't care who controls a wallet. And before you ask, what about AML, it's all anonymous, right? The issuer (e.g., Circle) is OFAC and FinCEN compliant, as is the custodian, and often the orchestrator and wallet.

So you could have a wallet that holds funds for 1000s of customers, then you figure out who owns what (this is how a lot of centralized crypto exchanges work today). Or you couldadd multi-wallet capabilities to create “virtual accounts” that:

You control for customers,

Customers control directly

Or some mix where customers control their money, but you can help out above, say $10k.

Wallets control the fund instructions. In principle it’s quite similar to the FBO or MTL models, but in practice,e this looks quite different

Where does the money sit in the stablecoin model?

Great question. Assets always “live” on the ledger, and wallets hold keys that give instructions to move assets. In a sense, every ledger can be a core ledger, an FBO account, and a subledger, if you have the right wallet and custody setup.

Who controls the keys controls the flow of funds

So where the money sits is onchain (solana, eth), but is managed via a wallet. There are numerous options for managing or securing that wallet.

Confusing? Yes. The upside: perfect transparency. The downside: you're responsible for your own security. We also have to manage multiple networks and stablecoins. That’s why orchestrators like Bridge and BVNK are seeing a lot of momentum. The complexity they hide is significantly more than the fintech folks did.

Stablecoins are more than just another rail

They’re a platform to build new financial products.

More efficient for FX (if we have local stables)

Global, 24/7 and instant

Programmable, meaning we can take new tokenized assets and construct new experiences

When you can create instant draw-downs against a private credit facility for a credit card program, you’ve crossed a line of financial efficiency that everyone is missing.

Instead of focusing on what this means for card networks and consumer payment volume, focus on the cost of goods sold (COGS) of the new players, and who’s using stablecoins to transform their margins in FX and banking.

The opportunity with stablecoins is to build entirely new financial products.

If you're at a bank: Stop thinking "stablecoins are just another rail." Start thinking "what products become possible with instant settlement?" Your competitors are building them now.

If you're building fintech: Every product you've ever wanted to build but couldn't because of settlement delays - build it now. The constraint is gone.

If you're investing: Look for companies solving problems that were impossible to solve profitably before instant settlement. That's where the alpha is.

BaaS created neobanks by removing licensing constraints. Stablecoins will create entirely new categories of financial products by removing settlement constraints. The companies being built in this unconstrained space won't just be better versions of existing products - they'll be products that couldn't exist before.

The constraint removal cycle continues.

The question isn't who dies - it's what becomes possible

ST.

4 Fintech Companies 💸

1. Polar - Stripe Billing for LLMs and modern SaaS.

Polar provides checkouts and complex billing like usage or subscriptions with a customer management and global merchant of record (MOR) capability built in. It also features an entitlements engine that grants buyers access to license keys, a GitHub repo, or Discord roles. Framework adaptaters aim to get customers up and running in under a minute.

🧠What Stripe was for accepting payments, Polar is for all of billing. It will automatically measure token consumption for AI Agents, or give precise measurements of execution time on a platform. It’s handing a lot of that messy measurement stuff which becomes a massive time saver for customers.

2. Nevermined - Billing for AI Agents

Nevermined simplifies billing for AI Agents with three pricing models for usage, outcome and value based pricing models. It manages metering and can handle human to agent or agent to agent payment requests. It combines its pay product with an ID product that logs every request, payout or policy change to trace billing and reduce error.

🧠This is about getting to revenue faster. Stripe Billing can do most of this stuff, but with a custom API for this use case, you get the type of metering and pricing models baked in that you’re most likely to need. Stripe has an almighty head start in this category, but its the kind of niche that could create room for many more winners.

3. Ivy - The Global Pay by Bank Aggregator

Ivy is creating a single API for pay by bank in multiple markets. Their goal is to create default global, default real time payments. They’re currently live in 28 countries and provide a single API to instruct pay outs or pay ins for clients like crypto exchanges, marketplaces and trading apps.

🧠Somebody needed to build this. Pay by bank is slowly becoming a normal thing in 60+ countries. There is no obvious aggregator API with mind share (albeit a lot of the open finance providers would be that, they’re not seen as payments companies). There’s value in being that category defining company sometimes.

4. NaroIQ - Whitelabel Fund infrastructure

Naro helps smaller firms build their own ETFs, offer other ETFs on firm infrastructure, and provides a suite of indexing solutions. Asset managers benefit from a much lower cost to create funds (than manually) as well as the ability to manage the lifecycle of ETF offerings to market.

🧠Blackrock iShares, Vanguard and Fidelity dominate the ETF market, there’s room for new players. I’d love to know what traction this team has, and what ETFs are being built on their platform.

Things to know 👀

1. Kalshi raises $185m at $2bn valuation. The Circle of Prediction Markets?

Kalshi just raised $185m at a $2bn valuation led by Paradigm. That's more than DOUBLE Polymarket's recent $1bn. Kalshi is a prediction market, like Polymarket, that lets users "predict" event outcomes from pop culture events to political. The news follows Bloomberg reports of Polymarket raising $200m at $1bn. Polymarket is often quoted by media commentators (notably during the last election).

🧠Polymarket has mindshare but can’t touch US users. The biggest prediction market in history... banned from its biggest market.Kalshi is CFTC-regulated and able to advertise to US customers. They’ve recently gone much harder on advertising and that’s driven a spike in user growth.

🧠The $1B gap reveals the real game. Paradigm didn't invest in gambling. They invested in the ability to predict outcomes for insurance, derivatives and any form of conditional payment.

🧠Prediction markets are often right when other forms of gambling or prediction are wrong. That's their superpower. They’re more useful when you want the best information about a likely outcome. That is their true utility.

🧠 There is an issue with consumer gambling regardless. Young westerners are gambling because the "legitimate" path to wealth feels rigged anyway. Same odds, different casino. That’s an issue. However, that puts prediction markets at the center of a larger social issue; it doesn’t make them the cause of that problem. And prediction markets do at least have major utility in financial markets.

🧠 If you pay attention to one signal make it this one. Matt Huang from Paradigm said “Prediction markets remind me of crypto 15 years ago: a new asset class on a path to trillions.” - Matt was super early in Bitcoin. When Matt says things like that. Listen.

Fiserv said in a press release it will launch its own stablecoin, “FIUSD will be powered by the infrastructure of Paxos and Circle, and targets interoperability with other stablecoins,” and will launch on the Solana network. Fiserv also plans to work with banks on deposit tokens

This from institutional blockstories is fascinating: End users will see a separate FIUSD balance in their banking app to reflect distinct custody and operational assumptions. On the backend, Fiserv is using Finxact to let banks subledger stablecoin holdings down to individual customers. Circle and Paxos are seen as complementary: Circle for deep USDC liquidity, Paxos for PYUSD interoperability.

🧠 Everyone needs a stablecoin story. Analysts are asking about it, its moving stocks, and so “announcing” something is smart PR.

🧠What do I need a “core” ledger for if I have stablecoins? There’s the small matter fo all of the assets in all of the world existing on existing core ledgers. If stablecoins are going to get liquidity that’s going to need to work well with the banking sector. Banks are becoming the ISPs of onchain finance.

🧠 Every bank would need new tech to work with their existing tech. Banks don’t replace their core in the same way you don’t replace your heart and brain in a single surgery. The existential risk is too high.

🧠Deposit tokens will find their place in the market. Onchain finance will need many funding models. Just as sponsor banks did very well in BaaS, the banks (and shadow banks) that lean into stablecoins will reap a massive opportunity.

🧠Paxos and Circle are strange bedfellows. Paxos is a major competitor to Circle, behind the USDG consortium (which Robinhood and Mastercard are a part of). It’s custodied in Singapore meaning it offers 4.1% yield.

🧠Compatibility with PYUSD is a sign of the thinking here. There’s an interoperability problem in stablecoins. Do this fix it?

🧠We’re at peak stablecoin PR surely. SoFi launched global remittances, the Visa CEO was on CNBC talking about them, Kraken launched “Krak” their stablecoin-only wallet to compete with PayPal / Wise etc.

Good Reads 📚

Jev gives an incredible breakdown of Coinbase’s new payments protocol used by Shopify for the acceptance of USDC in commerce payments.

The Commerce Protocol implements “authorization” (placement of a hold on buyer funds) and “capture” (distribution of payment to the merchant) by introducing an “Escrow” smart contract. At “authorization”, funds move from the buyer to the Escrow, and at “capture”, funds move from the Escrow to the merchant. The smart contract is controlled by an operator. In card terms: the blockchain acts as the scheme, the protocol defines the scheme rules, the “Operator” functions like a merchant acquirer, and the “Escrow” serves as the merchant processor.

🧠 Jev brilliantly contrasts how cards work vs how this protocol works. He gives examples like how an auth expires, vs an escrow contract sending funds back to a buyer if the merchant fails to “capture” funds.

🧠 “Token collectors” are a specific set of rules about how transactions are authorized. They work like a card scheme does. But in the cards world only a card scheme can define those rules. For Coinbase’s commerce protocol, there’s a lot more scope. Any issuer could be a token collector (e.g. Chase, Amex, Nubank), but would have much more scope over how things like chargebacks work.

🧠 Jev expects new issuers (token collectors) and merchant acquirers (operators) to emerge. But will they interoperate? If everyone can set their own fee will we get into a world where only some wallets work at some merchants? This is good for store-brand cards

🧠 This isn’t a competitor to card networks; it’s a competitor to ISO8583. The protocol that defines how a transaction works could reshape the value chain. It creates space for new networks, issuers and acquirers to emerge. As Rob Hadik argues, it could even collapse the value chain.

Tweets of the week 🕊

That's all, folks. 👋

Remember, if you're enjoying this content, please do tell all your fintech friends to check it out and hit the subscribe button :)

Want more? I also run the Tokenized podcast and newsletter.

(1) All content and views expressed here are the authors' personal opinions and do not reflect the views of any of their employers or employees.

(2) All companies or assets mentioned by the author in which the author has a personal and/or financial interest are denoted with a *. None of the above constitutes investment advice, and you should seek independent advice before making any investment decisions.

(3) Any companies mentioned are top of mind and used for illustrative purposes only.

(4) A team of researchers has not rigorously fact-checked this. Please don't take it as gospel—strong opinions weakly held

(5) Citations may be missing, and I’ve done my best to cite, but I will always aim to update and correct the live version where possible. If I cited you and got the referencing wrong, please reach out