Welcome to Fintech Brainfood, the weekly deep dive into Fintech news, events, and analysis. You can subscribe by hitting the button below, and you can get in touch by hitting reply to the email (or subscribing then replying)

Hey Fintech Nerds 👋

Stablecoin summer is in full swing. Circle is now valued at over $61bn, Shopify and Coinbase announced Coinbase Payments, and JP Morgan clapped back with its JP Morgan Deposit Token.

Everyone needs a stablecoin story. It’s clear that as the GENIUS bill passed through the Senate, there’s a lot of excitement, hype, and hyperbole. But underneath that, there’s real growth and innovation. During these moments, it’s important to take a breath and focus on the data. The data shows stablecoin usage for payments by businesses is growing 4x YoY.

But that’s all emerging markets, and all exotics. Useful, but not for the G20. That’s why I think the Shopify and Coinbase move is the biggest signal in all of the noise. Their Coinbase Payments is like the ISO8583 of stablecoins. A standard for managing payments, escrow and disputes. Like ISO8583, different card networks can “operate” this standard. And if it gets traction, it could truly disrupt commerce.

Consumer protections will come to all payment types. Your Rant this week is about Visa quietly adding chargebacks (and other rules) to pay by bank in Europe. Imagine that for stablecoins too? That’s your Rant for this week.

Here's this week's Brainfood in summary

📣 Rant: Pay by Bank has Chargebacks now.

💸 4 Fintech Companies:

Open Trade - Embedded Yield-as-a-Service for stablecoins

Opendue - The borderless account built on stablecoins

Teal - Atomic / Pinwheel for the UK

Payrails - Payment orchestration for global enterprises

👀 Things to Know:

Coinbase Payments with Shopify - A genuine Stripe competitor?

Weekly Rant 📣

Pay by Bank has chargebacks now.

Pay by Bank now has chargebacks. On the surface, this looks like Visa co-opting yet another fintech innovation. But zoom out and something more important is happening: everyone's racing to become the trust anchor for AI-driven finance.

A couple of weeks ago, Visa announced they’re adding “guarantees” for pay by bank transfers in the UK. Far from competing with card networks, its starting to look like pay by bank is becoming just another way for them to do what they do.

The DoJ intervening in Visa’s attempt to acquire Plaid feels like a lifetime ago, and with open finance in crisis as 1033 hangs by by a thread... I sense something like card network rules, and authentication will be crucial to open finance delivering on its potential.

If we’re going to get AI that can file our taxes, manage investments, and run payment ops for a business, we have some massive trust problems to solve. To do that, we need a compelling link between the consumer, the business, their account, and their consent.

I call that the trust anchor.

And the next decade of open finance, in fact, all of finance, will be defined by who gets to become that anchor.

The Visa move changes everything.

Pay by bank was quietly building momentum, but missing a “crossing the chasm” moment, and a better user experience could be the thing that does it.

If there was one sell-out topic at Money 2020 Europe (aside from stablecoins and agentic commerce) it was open finance, and, specifically, pay by bank. The big driver is major PSPs like Adyen, which have now made pay by bank an option at checkout.

To a consumer, pay by bank isn’t some weird new thing, it’s now that other thing sitting there. To a merchant pay by bank isn’t a new integration, it’s just another option from their PSP that might improve conversion/retention. As one exec working in open finance said to me:

Our month-over-month volumes are doubling every month and have been doing so for the past year. That’s from a low base, but it’s starting to get very meaningful.

This is the beginning of mainstream adoption, but not the end. The UX is still jarring, and the lack of consumer protections is a genuine concern. The problem has been and still is, there’s no clear pattern for pay by bank. For the consumer, or merchants. That experience of paying, and it working is a really tough nut to crack.

Now throw a simple, consistent user experience over the top of that, and you’re adding fuel to the fire. Pay by bank has, for a long time, been inconsistent and janky. Wait, so I click this new logo, and it wants a QR code, then I connect via my bank app.

Card-based rules + open finance could be just that.

And open finance has one major advantage that traditional card rails lack.

The Data Advantage unlocks Agentic Payments

Pay by bank has one massive advantage over the traditional card networks that doesn’t get talked about enough. The ability to have the data about the account travel with the transaction. That helps us with all kinds of issues like “are there enough funds to make this payment,” and “is the recipient a known scammer?” It even opens up some fascinating loyalty and reward possibilities.

Secure, consumer permissioned connectivity to an owned, KYC’d bank account can become a powerful trust anchor in commerce and recurring payments. If a payment or subscription is initiated via that consumer's permissioned consent, it can also be revoked, managed, or otherwise directed.

The connectivity between consumer → consent → AI agent → action has untapped potential today, but in the age of AI it will be critical.

I consent to my AI overlords running my finances thank you

Imagine a future where an AI Agent is managing your subscription, calculating taxes, optimizing your wealth strategies. How is all of that being anchored back to an underlying account and an underlying permission?

So much of the “agentic commerce” conversation is focussed on payments, but frankly, payments are just one type of permission, consent or mandate. There are many others, like submit my tax return,

Why? Because when we have AI Agents managing subscriptions, we’re going to want to be able to audit who they are, and what they do before anything happens.

Visa and Mastercard have agent tokenization initiatives; they also have their “flex credentials,” which means a tap or auth can be an authentication for anything. Increasingly, the card networks are trusted “authorizers” of things like payments, proof of age, and AI agents.

But authentication is only one part of the story. Mandates, consent, and permissions are complex.

The roadmap for open finance is fascinating, because it’s a programmable link back to a known identity with permissioning built into it. And that could be even more interesting in B2B.

Pay by Bank for B2B is right there for the taking.

AI Agents with bank-grade data could automate countless complex workflows for businesses. A lot of workflows you see inside modern tools like Ramp or Brex become available to companies with multiple accounts across multiple banks. Here’s a handful of things we will start to see.

Agents run payment ops (e.g., Payman AI), trained on the NACHA handbook

Agents reconcile invoices across multiple bank accounts

Agents flag unusual vendor payments before they happen

Agents negotiate payment terms based on real-time cash flow from multiple accounts

Agents manage your cashflow waterfall across checking, deposits, MMFs and yield

You could see these agents as start-ups or embedded inside the existing operating systems of growth companies (again, your Ramp, Brex, Mercury types).

The core insight is that businesses rarely have one account. As they scale, they get more, and their workflows across those become increasingly complex. So you need Agents that can operate across that estate, with consent and permissions, and open banking is perfectly set up to do that.

Now layer on the spike of fraud and scams, specifically targeting businesses and the fact that AI Agents are worryingly easy to attack with prompt injection, and the need for that trust anchor back to a consent and permission becomes even more important. As Simon Willison points out, we're heading toward a 'lethal trifecta' where AI agents have access to money, can be fooled by bad actors, and operate at machine speed. Without cryptographically secure permission frameworks, we're building the world's most efficient fraud machine

The future of open finance is the identity and authentication layer.

Open finance provides us with ground truth from a KYC’d account through to every other type of financial transaction. There are many types of transactions beyond a payment, albeit, the payment is often the most important and first use case we see.

Pay by bank today lacks consumer protection or a consistent experience. That was a logical place for the card networks, which have perfected those elements to start.

But today, there is so much value on the table with open finance. And tomorrow it becomes almost unlimited.

So who wins the race to become the trust anchor for AI-driven finance?

The Contenders:

Card Networks: Have the infrastructure, consumer trust, and dispute resolution

Open Banking Aggregators: Have the data advantage and direct account access

Big Tech: Have the users but face regulatory headwinds

Banks: Have the accounts but move at glacial pace

Startups: There’s a whole category of “Plaid for memory” start-ups emerging that help remember everything about you to make LLMs better.

My bet? It's not winner-take-all. We'll see partnerships and co-opetition. Visa's move in Europe is just the first step..

Open Finance’s next decade.

By 2035, we’ll have AI Agents driving a substantial portion of economic activity.

In that world, we need a trust anchor and a consent framework. Open Finance (and open data more broadly) is almost ideally positioned to be that trust anchor.

The company that controls this trust layer wins more than a payments battle. The winner becomes the infrastructure for the entire AI economy. Every automated subscription, every

agent-negotiated contract, and every AI-driven financial decision flows through their rails.

That's the real prize everyone's racing for.

ST.

4 Fintech Companies 💸

1. Open Trade - Embedded Yield-as-a-Service for stablecoins

Open Trade provides embedded stablecoin yield for fintech companies who want to offer that to their customers. Open Trade handles off-chain banking, asset custody, and manages bankruptcy remote SPVs to ensure asset safety. Open Trade also handles the on-chain connectivity to the ethereum ecosystem, so a Fintech company has less technical complexity to manage.

🧠 If every company is becoming a stablecoin company, open trade is how they add yield. Think about the amount of treasury management Fintech companies that now offer money market funds (e.g. Mercury, Ramp, Brex, Meow, the list goes on). Now consider that Ramp is going into 120 more markets via stablecoin financial accounts. Wherever the stablecoin goes, the yield can follow. And like that you begin to see the value of a composable stack.

2. Opendue - The borderless account built on stablecoins

Opendue helps companies receive, hold and send dollars and euro’s “from anywhere.” The company is targeting global treasury management, import/export, companies in e-commerce selling globally, marketplaces, travel and gaming.

🧠Get dollars “anywhere” shows the promise and the risk. The amount of companies who come into the global economy and the GDP unlock here could be truly incredible to witness. But “anywhere” includes Russia and Iran, which OFAC may have something to say. It’s encouraging to see Opendue lists blockchain analytics startup Elliptic as one of its partners which indicates good understanding. (Their partner list is in fact, very revealing about how the whole stack is built if you know what you’re looking for).

3. Teal - Atomic / Pinwheel for the UK

Teal provides income verification to allow lenders to underwrite new customers with user permissioned access to payslips. This can also be done over time or on a monthly basis (e.g. for workers in the gig economy who may have choppy incomes).

🧠It’s hard to understand how much of a gap this is in the UK fintech ecosystem. Long over due. Teal have been griding at getting this right for a short while but appear to be finding traction. Worth a look UK fintech folks.

4. Payrails - Payment orchestration for global enterprises

Payrails helps merchants and marketplaces route payments to different PSPs, optimize transactions with custom workflows, and automate manual work (like reconciliations). It has analytics designed to help payments teams boost conversion and become much more global by creating a single payments hub.

🧠Payment orchestration felt like all the rage in ‘22, ‘23 but is making a comeback. Payrails has some impressive logos like Puma, Vinted and “Uber for the middle east” Careem. It’s one thing to orchestrate multiple PSPs and create workflows, its another thing to focus on helping companies with market expansion and revenue growth. I wonder how stablecoins would change this picture if at all?

Things to know 👀

1. Coinbase Payments with Shopify - A genuine Stripe competitor?

The Commerce Payments Protocol launching on Shopify establishes the first standardized messaging format for programmable money. Complete with consumer protections. It has a

A checkout that can accept stablecoins

A commerce layer (that handles auths, refunds, ledgering, subscriptions)

A protocol layer (that handles escrow, on-chain transactions and refunds)

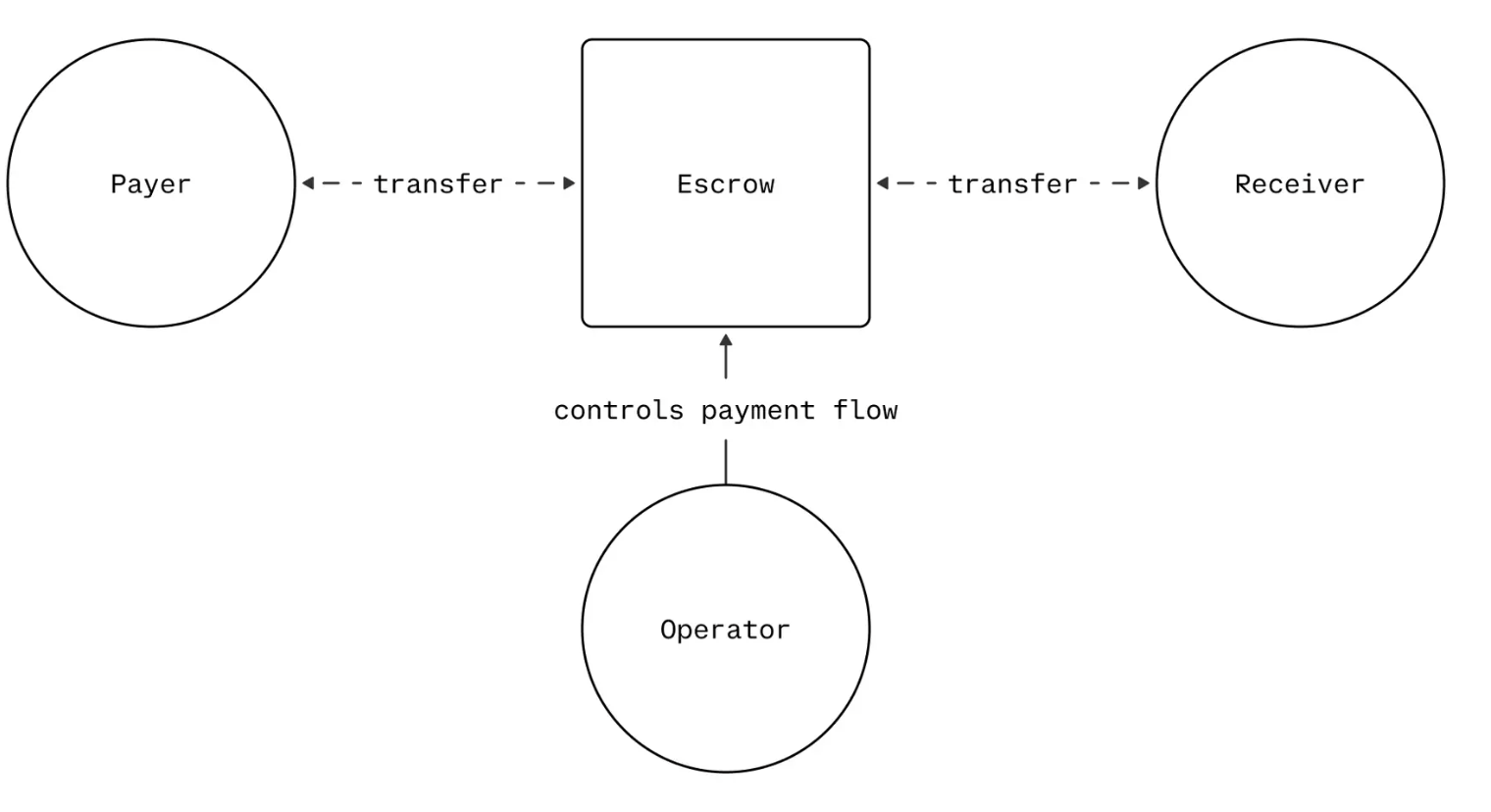

🧠A genuine alternative to “auths” from card networks. The commerce protocol moves buyer funds into an escrow contract on “auth” and then to the merchant on “capture.” There’s a third “operator” role (equivalent to a card network) that helps ensure payments happen.

The Escrow + Operator entity model

🧠A genuine alternative to ISO8583 someday? If stablecoins do take off for commerce, we will need consumer protections. The protocol includes protections like void, return and reclaim. It’s well worth a read of the developer blog. I could imagine an existing card network, as well as new ones playing the “operator” role.

🧠Coinbase has the full stack.

They’re a major beneficiary of the USDC stablecoin

They have a dedicated L1 (base) that captures fees for payments

They offer self-custody wallets for merchants and consumers

Now they’re building “embeddable” PSP-like capabilities that Stripe made famous

But it’s on-chain native only

🧠Is this a genuine competitor for Stripe? Shopify was always the canonical Stripe test-case client. Coinbase is clearly further ahead in stablecoins but Stripe has Bridge which manages stablecoin pay-ins, payouts and settlement, and Privy that’s a self-hosted wallet. Stripe also has TradFi rails and a lot more distribution. This could be an interesting battle to watch.

🧠 What this actually does is collapse multiple roles. The scheme, acquirer, and processor are all now in the “operator” role.

🧠 The only thing they don’t do is support traditional rails as seamlessly as Stripe. It looks like Stripe is quietly helping a lot of things, like cashback and seamless merchant payouts, happen behind the scenes in this Shopify / Coinbase setup. On-chain + off-chain + distribution could be a killer combo.

Want to dig in more? Here’s a great tweet.

One of the world's largest banks is going on chain, with a deposit-backed token on the base network (the Ethereum L2 built by Coinbase). Positioned as an alternative to stablecoins, “JPMD” is a deposit token designed to offer many of the benefits of being on chain, but being linked to commercial bank money (which offers FDIC insurance). This token is “permissioned” (only available to JP Morgan’s institutional clients). They expect it to be used for on-chain digital asset settlement and cross-border payments.

🧠This is clearly aimed at corporate treasurers who are stablecoin curious. Unquestionably, JP Morgan will have been getting questions “will you support stablecoins?” - “Can I use stablecoins through you?” This is their answer.

🧠 This is a compelling pitch to large corporates. Kinexsys + JPMD offers many of the benefits of stablecoins + backward compatibility with the banking system.

🧠 The downside of Kinexsys is that it is closed loop.

Kinexsys moves TRILLIONS annually, cross-border, 24/7 (it's actually insane)

But it's like having the world's fastest car that only works on one highway

Stablecoins work everywhere. That's the point.

🧠 Stablecoins are a bottom up alternative that have expanded the TAM of payments. That’s why Stripe is investing so heavily, and volume growth is explosive.

🧠 Why launch JPMD on base if they have Kinexsys? JPMD is intended for wider use than institutional. Over time JPMD could compete with USDC or USDT for dollar usage as on chain finance grows in consumer and commercial payments use cases.

🧠 Every other bank will now try to copy this. They’re getting the same stablecoin questions from their clients and will wake up to this headline.

Revolut, the neobank with 50M customers, is quietly building its own stablecoin according to Decrypt. The moves follow the launch of a dedicated crypto exchange (Revolut X), and its long-standing support for crypto trading and swaps in its core app. Why could this make sense?

🧠Revolut grew up in FX. The CEO (a former FX trader) likely sees at minimum an internal treasury use case to manage cash building up in long-tail markets.

🧠Revolut is also growing in the global south. Payouts, pay-ins, and stablecoin-linked card transaction volume are booming.

🧠The treasury, then the payout path, is becoming common. I spoke to the CRO of Dlocal on the Tokenized podcast (episode drops Monday). He told me they’d been using stablecoins to manage treasury for the past 4 years quietly. Both Dlocal and WorldPay have recently added payout capabilities following customer demand. Which tells you everything about where the value is right now.

Good Read 📚

LLMs are incredibly easy to prompt inject. The problem is that they follow instructions in the content, and with external communication, they have hundreds of possible entry points for content payloads that are harmful.

🧠 This is the next cloud security issue waiting to happen x 100. If everyone runs on AI Agents, and those AI Agents are easy to inject with malicious content, we have a problem.

🧠 We’re already seeing agents run in sandboxes for commerce, I expect they’ll need to for enterprise too. Open-loop agents just using your internal systems feel dangerous to the point of being irresponsible. Genuinely worry about a lot of these “Agentic” workforce replacement drives your legacy system of record companies…

Tweets of the Week 🕊️

That's all, folks. 👋

Remember, if you're enjoying this content, please do tell all your fintech friends to check it out and hit the subscribe button :)

Want more? I also run the Tokenized podcast and newsletter.

(1) All content and views expressed here are the authors' personal opinions and do not reflect the views of any of their employers or employees.

(2) All companies or assets mentioned by the author in which the author has a personal and/or financial interest are denoted with a *. None of the above constitutes investment advice, and you should seek independent advice before making any investment decisions.

(3) Any companies mentioned are top of mind and used for illustrative purposes only.

(4) A team of researchers has not rigorously fact-checked this. Please don't take it as gospel—strong opinions weakly held

(5) Citations may be missing, and I’ve done my best to cite, but I will always aim to update and correct the live version where possible. If I cited you and got the referencing wrong, please reach out